Still Justify Its High Price After Recent Share Gains?")

If you are wondering whether Tesla’s share price still reflects the story you have in mind, this article focuses on what the current market price might imply about the company’s value. Tesla recently closed at US$376.02, with returns of 3.9% over 30 days, a 28.8% gain over 1 year, 134.6% over 3 years, and 67.5% over 5 years. Year to date the stock is down 14.2%, and over the last 7 days it has declined 2.7%. Recent headlines have continued to focus on Tesla’s role as a major electric vehicle and technology company. This includes ongoing attention on its product roadmap, competition in EV markets, and management decisions that can influence sentiment around the stock. Media coverage of these themes often gives investors new information to weigh against the share price moves described above. Tesla currently has a valuation score of 0 out of 6. The rest of this article will walk through common valuation approaches while highlighting a more complete way to think about value that will be covered at the end.

Tesla scores just 0/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Tesla Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a business could be worth by projecting its future cash flows and then discounting those back into today’s dollars using a required rate of return.

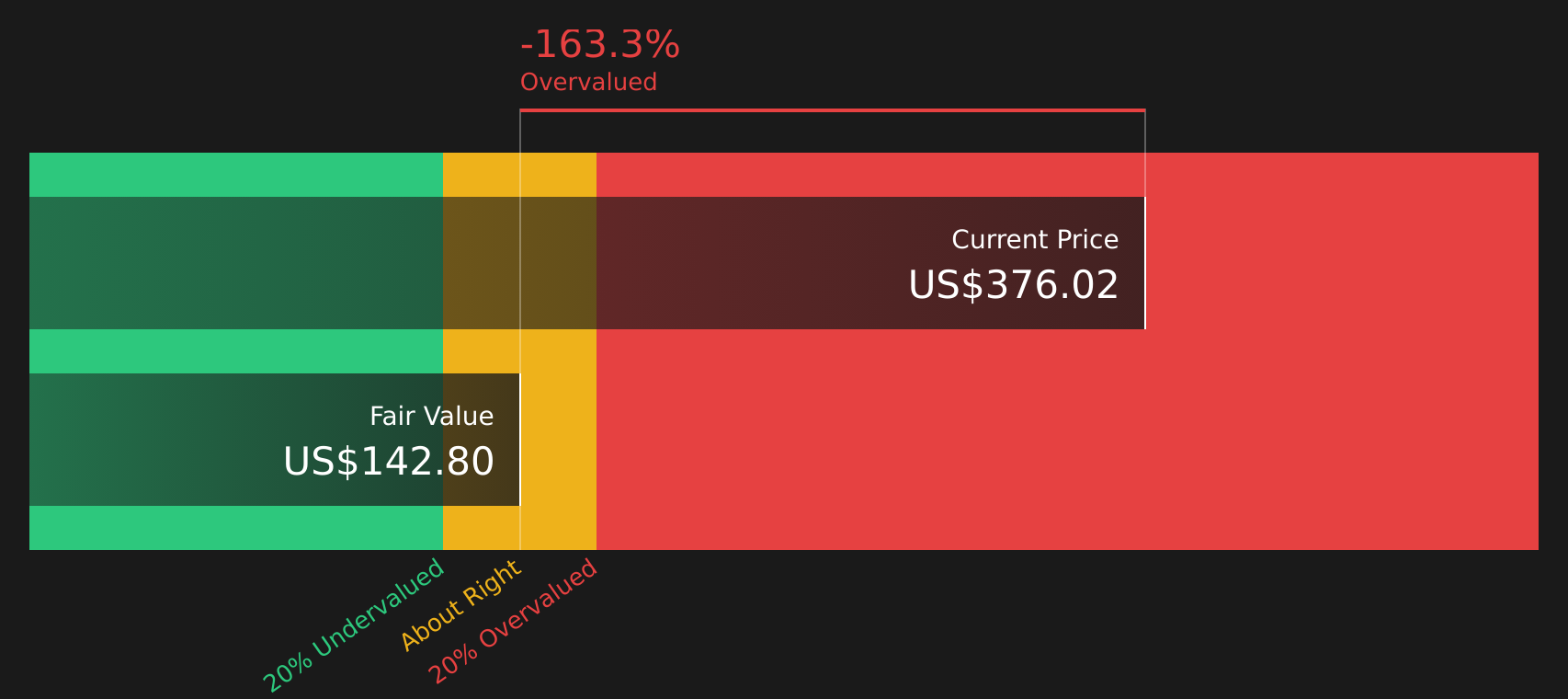

For Tesla, the model used here is a 2 Stage Free Cash Flow to Equity approach based on cash flow projections. The latest twelve month Free Cash Flow is about US$6.6b. Analyst estimates and extrapolated figures extend out to 2035, with projected Free Cash Flow for 2030 at roughly US$22.8b and higher extrapolated figures in the following years.

Simply Wall St discounts each of these annual cash flows back to today and adds them up to arrive at an estimated intrinsic value per share of US$142.80. Compared with the recent market price of US$376.02, the model suggests Tesla trades at a 163.3% premium to this DCF estimate, which points to a rich valuation based purely on these cash flow assumptions.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Tesla may be overvalued by 163.3%. Discover 53 high quality undervalued stocks or create your own screener to find better value opportunities.

TSLA Discounted Cash Flow as at Apr 2026

TSLA Discounted Cash Flow as at Apr 2026

Approach 2: Tesla Price vs Sales

For companies where investors focus heavily on revenue potential, P/S can be a useful gauge of how much the market is willing to pay for each dollar of sales. It is often applied to businesses where earnings can be volatile or less reflective of the long term story.

Growth expectations and risk both influence what looks like a normal P/S multiple. Higher expected growth or stronger perceived competitive position can support a higher P/S, while higher risk or weaker profitability can justify a lower one.

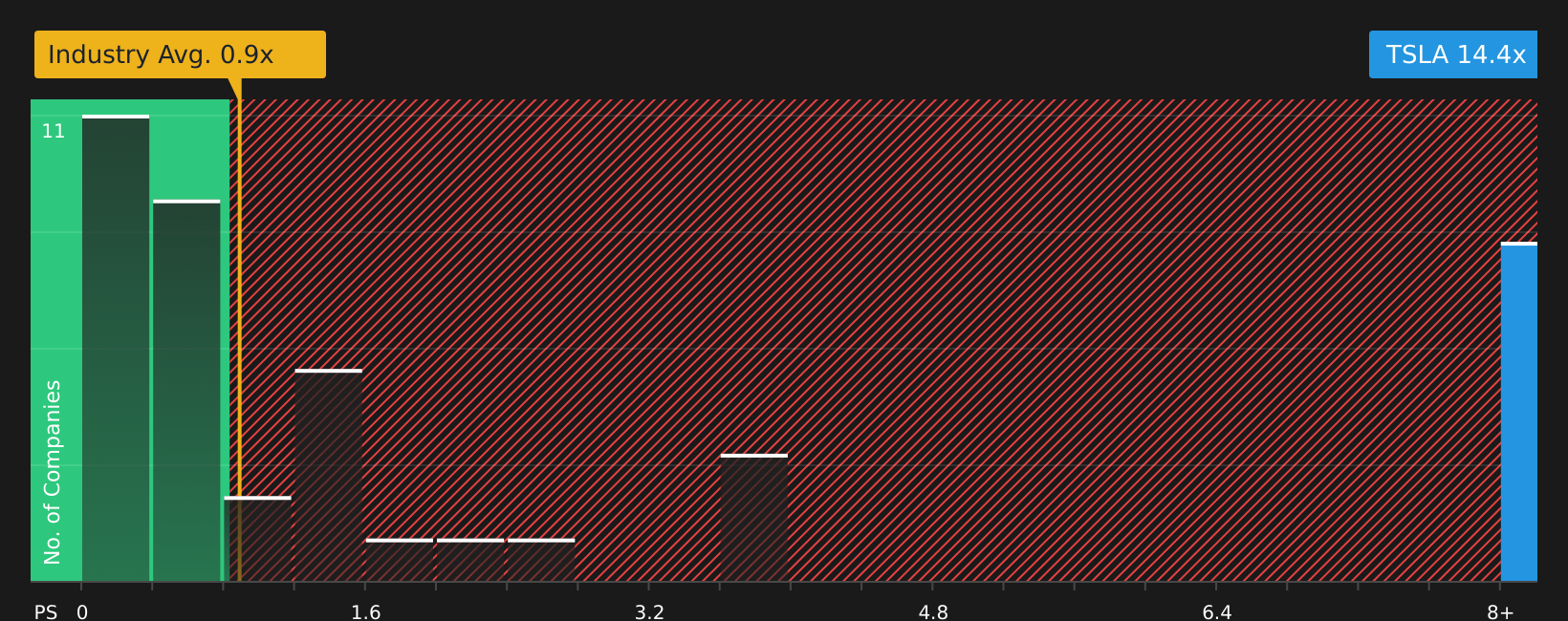

Tesla currently trades on a P/S of 14.43x. This is well above the Auto industry average P/S of 0.88x and also above the peer group average of 1.39x. Simply Wall St’s Fair Ratio for Tesla is 3.15x. This is a proprietary estimate of the P/S multiple that might be reasonable given factors such as earnings growth, industry, profit margins, market cap and specific risks.

The Fair Ratio is more tailored than a simple comparison with peers or industry averages because it attempts to adjust for company specific traits instead of assuming all Auto companies should trade on the same multiple. Comparing Tesla’s actual 14.43x P/S with the 3.15x Fair Ratio suggests the shares trade at a richer level than this framework implies.

Result: OVERVALUED

NasdaqGS:TSLA P/S Ratio as at Apr 2026

NasdaqGS:TSLA P/S Ratio as at Apr 2026

P/S ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 18 top founder-led companies.

Upgrade Your Decision Making: Choose your Tesla Narrative

Earlier this article pointed to a richer way to think about value, and this is where Narratives come in, letting you connect your own story about Tesla to a financial forecast and a fair value instead of starting from a single label like overvalued or undervalued.

A Narrative on Simply Wall St is your view written into numbers, where you spell out how you see Tesla’s future revenue, earnings, margins and risks, then see what fair value that story implies and how it compares with today’s US$376.02 share price.

Because these Narratives live inside the Community page and update as new news, earnings and analyst estimates arrive, they give you an accessible way to keep your Tesla thesis current while the platform used by millions does the recalculation work for you.

They can also help you decide how to act on valuation by lining up Fair Value next to Price so you can see, for your story, whether Tesla looks expensive, cheap or roughly in line and how that has changed as the facts have shifted.

Looking at existing Tesla Narratives shows how wide the range of reasonable stories can be, from fair values around US$69 or US$75 at the low end to figures near US$2,500 at the high end, with others clustered between roughly US$175 and US$665, and Narratives give you a clear framework to see where your own view sits in that spread.

For Tesla however we will make it really easy for you with previews of two leading Tesla Narratives:

Fair value in this bullish narrative: US$2,707.91 per share

Implied discount to this fair value at US$376.02: around 86% below the narrative estimate

Assumed revenue growth used in the model: 77%

This thesis treats Tesla as a broad technology platform across AI, robotics, energy, software and vehicles, not just an automaker. It aggregates multiple revenue streams through 2030 and applies P/E based scenarios to estimate a current fair value in the low thousands per share. The author flags sizable execution, competition and regulatory risks but still sees a large potential payoff if Tesla reaches the scale outlined.

Fair value in this more cautious narrative: US$322.21 per share

Implied premium to this fair value at US$376.02: around 17% above the narrative estimate

Assumed revenue growth used in the model: 18%

This story focuses on Tesla’s AI compute, self driving and energy storage opportunities, paired with more moderate growth and profitability assumptions. It values the company using revenue based multiples, with an explicit focus on how Dojo, FSD, Megapacks and services might scale against capacity and policy support. The author highlights key operational and technology risks, including sensor choices and execution on autonomy, which keep the fair value closer to the current price.

If neither of these fully matches your own expectations for Tesla’s future, that gap is where a custom Narrative can help you put your view into numbers instead of relying only on labels like overvalued or undervalued.

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Tesla on Simply Wall St. Add the company to your watchlist or portfolio so you’ll be alerted when the story evolves.

Do you think there’s more to the story for Tesla? Head over to our Community to see what others are saying!

NasdaqGS:TSLA 1-Year Stock Price Chart

NasdaqGS:TSLA 1-Year Stock Price Chart

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we’re here to simplify it.

Discover if Tesla might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com