2026 looks set to be a year of anticipation rather than decisive change for ELV recycling. With the EU’s ELV Regulation still some way from finalisation, authorised treatment facilities will instead grapple with rising dismantling costs, more complex vehicle streams, raw material volatility and intensifying pressure from informal operators and larger market players.

Adam Małyszko

Adam Małyszko

With Europe’s long-awaited End-of-Life Vehicles Regulation (ELVR) still at least a year away from finalisation, and with implementation timelines stretching its real impact even further, 2026 is shaping up as a period of transition rather than transformation for the sector. Adam Małyszko, President of the Association of Car Recycling (FORS) in Poland, discusses how recyclers must navigate rising costs, shifting vehicle streams, market imbalances and intensifying competition in the meantime, as operational realities continue to evolve ahead of regulatory clarity.

For several years, in Europe, including Poland, the automotive recycling industry had been expecting changes related to the replacement of Directive 2000/53/EC dated September 18, 2000. A preliminary agreement on the basic content of the ELVR was reached at the end of last year, but we won’t see the final text until mid-2026 at the earliest. Given the transitional periods for applying the regulations, this document will have an impact on the market in more than three years. Until then, we must focus on what happens in the industry. In my opinion, a lot will be happening in each of the following four areas:

Types of vehicles for dismantling – dismantling costs

ELV entities – will small businesses survive?

Vehicle dismantling parts – market globalization

Prices of raw materials obtained from vehicle dismantling – impact on the economic result at ATFs

Types of vehicles for dismantling – dismantling costs

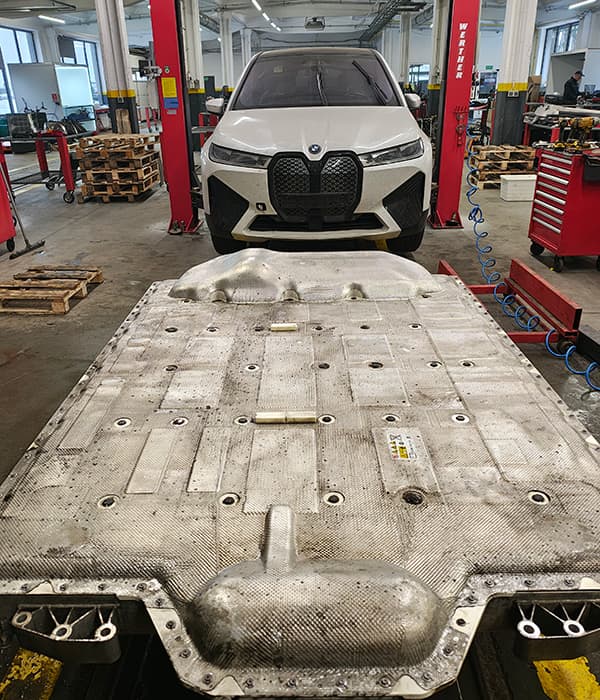

The vehicle dismantling market changes every year. In Poland, as in other European countries, we see increasing amounts of hybrid, electric, and even hydrogen vehicles. All of these vehicles are packed with electronics, numerous batteries, and other electronic control systems.

Electric vehicles are also heavier, which affects the amount of materials produced and the need to invest in additional equipment for ATFs, such as stronger lifts, forklifts, and additional fire protection. This directly impacts the profitability of dismantling companies. There is also a growing need for workers with electronics knowledge rather than for those with basic mechanical skills. Therefore, we must compete with employers who hire such specialists at authorized service centers for new car manufacturers.

This rapidly raises the costs of operating ATFs. It’s also impossible not to notice the increasing number of vehicles manufactured in China. However, they don’t reach dismantling sites in significant quantities in Poland, so we have no experience selling these parts or the raw materials we acquire. This doesn’t mean, of course, that we aren’t preparing for such dismantling. As I’ve been pointing out for years, the number of vehicle types and models submitted for dismantling is constantly increasing, necessitating continuous staff training. We spend a lot of valuable time dismantling various types of batteries, which we remove not only to sell them or comply with legal requirements, but primarily to prevent fires. This situation results in a growing list of parts that, despite being functional, we don’t dismantle and don’t sell for economic reasons.

One of the most serious barriers to vehicle recycling and the circular economy is the electronic blocking of parts by vehicle manufacturers. Even when parts are in perfect condition and suitable for reuse, digital restrictions can prevent their reuse. Car recyclers have been raising this issue loudly for years, but the problem continues to worsen.

ELV entities – will small businesses survive?

The automotive industry in Europe is experiencing a significant slowdown. Employees in this sector are increasingly being laid off or transferred to other roles.

Vehicle producers are therefore attempting to organize vehicle dismantling using infrastructure and staff previously used to produce cars. In Europe, we have a free flow of materials and services, so we have no basis to block these initiatives. Do they threaten existing vehicle dismantling companies? Yes, because producers want to control the raw materials used in vehicles and directly influence the types and volumes of parts recycled. This could crush existing entities, legally dismantling vehicles. On the one hand, there is a vast “gray market” that the authorities in many countries tolerate; on the other hand, there are powerful, technically organized corporations. So, this is a real threat that every vehicle dismantler in Europe should be aware of. In Brazil, for example, where the gray market is even larger than in Poland, car manufacturers have already begun piloting ATFs. EU and national regulations, environmental requirements, bureaucracy, uncontrolled competition and the threat from large corporations have already caused some entrepreneurs to abandon this type of business.

Vehicle dismantling parts – market globalization

Vehicle dismantling parts are increasingly being offered on global markets. One such example is the Lithuanian startup OVOKO, whose website currently offers 37,800,090 used parts from 6,540 entities. This wouldn’t be remarkable unless the vast majority of these parts did not come from legal dismantling. This results not only in price variations related to the country of origin, but primarily in price variations caused by vehicles dismantled of unknown origin and outside legal entities, including vehicles stolen in Western Europe and dismantled in Eastern Europe. Customers buying parts don’t see this difference; what matters is price, quality, and delivery time. Using parts of unknown origin to settle vehicle claims can also be very dangerous. The current situation means that legal companies are unable to adjust their prices to theoretical market prices and are increasingly less competitive compared to the gray zone, which has developed significantly in some countries.

Raw materials obtained from vehicle dismantling – price volatility

Raw materials obtained from dismantled vehicles are still a crucial source of income for ATFs. Currently, raw material prices are relatively stable. Prices of ferrous and non-ferrous metals, catalytic converters and batteries guarantee very good profitability with cost-free acquisition of end-of-life vehicles.

Unfortunately, the market doesn’t work that way; to obtain a vehicle for dismantling, you have to offer the customer a sufficiently high price. In countries where the gray zone market is quite small, the competitive mechanism operates, and companies consider the costs associated with legal operations when submitting bids.

Unfortunately, in many countries, including Poland, there is a large gray market that, due to its significantly lower operational costs, can offer a higher price for a vehicle for dismantling. Therefore, raw material prices do not directly impact the economic performance of ATFs, because higher raw material prices increase the cost of purchasing a vehicle for dismantling. In Poland, insurance companies take advantage of this situation by offering vehicles with significant damage, even completely burned ones, to entities not authorized to collect end-of-life vehicles.

Therefore, legals often lose. Another issue is electric vehicle batteries – everyone is seeking them as a source of valuable raw materials, but on the other hand, buyers are unwilling to offer any price and demand even additional payment for collecting them. For many of these batteries, disposing of non-reusable ones will have a negative economic impact on ATFs.

To sum up, until the new EU ELV Regulation comes into full force, which may provide some support to legal entities, the situation for ATFs will deteriorate.

Regulations defining the point at which a vehicle becomes an ELV, and the obligation to identify the origin of dismantled parts (VIN numbers), may help. Unfortunately, this will take over two years. However, there is still no solution to promote the transfer of vehicles to legal businesses. Further obligations imposed on legal entities mean further distortion of competition. Keeping this in mind, we will be watching the operations of the first dismantling station built in Poland by a manufacturer (TOYOTA) with great interest.

It’s possible that only the producer’s experience will lead to a better understanding of the situation in Poland’s vehicle recycling industry.

Further Reading on Auto Recycling World