Europe Electric Vehicle Charger Market Size

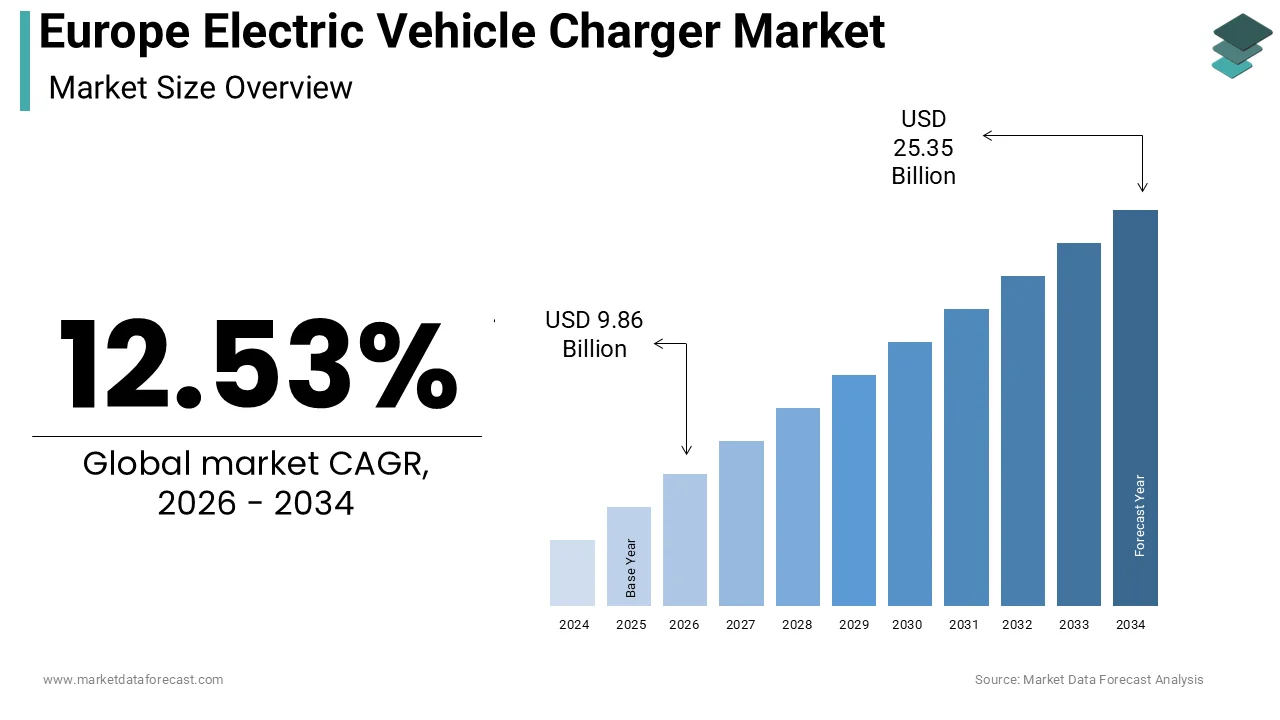

The Europe electric vehicle charger market size was calculated to be USD 8.76 billion in 2025 and is anticipated to be worth USD 25.35 billion by 2034, from USD 9.86 billion in 2026, growing at a CAGR of 12.53% during the forecast period.

An electric vehicle charger constitutes the critical infrastructure network enabling the transition from internal combustion engines to battery electric mobility. This ecosystem encompasses alternating current and direct current charging stations deployed in residential, commercial, and public domains. The strategic imperative for this infrastructure stems from the urgent need to decarbonize transport sectors in alignment with continental climate goals. As per the European Environment Agency, transport accounts for approximately 25% of total greenhouse gas emissions in the European Union, making electrification a pivotal strategy for mitigation. The proliferation of charging points is not merely a commercial endeavour but a regulatory necessity driven by the Alternative Fuels Infrastructure Regulation. According to the European Commission, member states must ensure that publicly accessible recharging points are installed at regular intervals along the core trans-European transport network by 2025. This regulatory framework mandates a minimum output power of 150 kilowatts for heavy-duty vehicles and 400 kilowatts for light-duty vehicles at specific nodes. The current landscape reflects a fragmented yet rapidly consolidating industry where interoperability and user experience remain paramount. Data from the European Alternative Fuels Observatory indicates that the number of publicly accessible charging points in the European Union reached 630,000 in late 2023. This growth trajectory underscores the intense focus on expanding coverage to alleviate range anxiety and support the anticipated surge in electric vehicle adoption rates across diverse geographical and demographic segments within the region.

MARKET DRIVERS Stringent Regulatory Mandates Accelerate Infrastructure Deployment

The imposition of rigorous legislative frameworks is a primary catalyst for the expansion of charging infrastructure across Europe. The European Union has enacted the Alternative Fuels Infrastructure Regulation, which sets binding targets for member states to install sufficient charging capacity. This regulation requires that by 2025, each member state must have a total output power of at least 1.3 kilowatts per battery electric light-duty vehicle registered. For plug-in hybrid electric light-duty vehicles, the requirement stands at 0.8 kilowatts per vehicle. These precise metrics compel governments and private entities to accelerate installation rates to avoid non-compliance penalties. According to the International Energy Agency, achieving global climate goals necessitates the installation of approximately 15.5 million public charging points by 2030. The regulatory pressure is further intensified by national bans on the sale of new internal combustion engine vehicles scheduled for 2035 in several key markets. This legislative certainty provides investors with the confidence required to commit capital to long-term infrastructure projects. Furthermore, the Fit for 55 package aims to reduce net greenhouse gas emissions by at least 55% by 2030 compared to 1990 levels. As per Eurostat, the share of renewable energy in transport reached 12.1% in 2023, highlighting the substantial gap that electric mobility must fill. Consequently, the regulatory environment acts not just as a guideline but as a forcing force driving the rapid scaling of charging networks to meet legally binding environmental and infrastructural benchmarks.

Escalating Consumer Adoption of Battery Electric Vehicles

The surging uptake of battery electric vehicles among European consumers fundamentally drives the demand for robust charging solutions, which is another major factor propelling the European electric vehicle charger market growth. Sales data indicate a profound shift in consumer preference towards zero-emission mobility options. According to the European Automobile Manufacturers Association, battery electric cars accounted for 14.6% of all new car registrations in the European Union in 2023. This represents a significant increase from previous years and signals a mainstream acceptance of electric technology. The growing fleet of electric vehicles creates an immediate and pressing need for accessible charging infrastructure to support daily usage patterns. Range anxiety remains a critical concern for potential buyers, and the availability of reliable charging stations directly influences purchase decisions. As per a survey by Deloitte, 60% of European consumers cite the lack of charging infrastructure as a major barrier to electric vehicle adoption. To address this, automakers and energy companies are collaborating to expand networks. For instance, Volkswagen Group plans to install 18,000 high-power charging points in Europe by 2025. The correlation between vehicle sales and infrastructure deployment is evident in markets like Norway, where electric vehicles comprised over 82% of new car sales in 2023, supported by one of the highest densities of charging points per capita globally. This dynamic illustrates that consumer demand is not passive but actively shapes the market landscape, forcing stakeholders to prioritize user convenience and network density to sustain the momentum of electric mobility adoption across the continent.

MARKET RESTRAINTS Inadequate Grid Capacity and Stability Concerns

A significant restraint impeding the growth of the European electric vehicle charger market is the limited capacity and stability of the existing electrical grid. The widespread adoption of high-power charging stations places immense strain on local distribution networks, particularly in urban areas with aging infrastructure. According to the European Network of Transmission System Operators for Electricity, integrating millions of electric vehicles requires substantial upgrades to prevent grid congestion and voltage fluctuations. Many rural and semi-urban regions lack the necessary transformer capacity to support multiple fast charging units simultaneously. This limitation forces utility companies to invest heavily in grid reinforcement before new charging stations can become operational. As per a study by the European Commission, the total electricity demand from electric vehicle charging is expected to increase to 15% of the European Union’s total consumption by 2050 if not managed properly. Such spikes threaten grid stability and may lead to blackouts or require costly real-time balancing measures. Furthermore, the intermittent nature of renewable energy sources complicates the integration process. Without adequate storage solutions or smart charging mechanisms, the grid struggles to accommodate the variable load profiles associated with electric vehicle charging. This infrastructural bottleneck delays project timelines and increases capital expenditures for charge point operators. The need for coordinated planning between grid operators, municipalities, and charging providers becomes paramount to ensure that the electrical backbone can support the anticipated load. Until these grid constraints are addressed through targeted investments and technological innovations, the pace of infrastructure rollout will remain constrained by physical and technical limitations.

Complex Permitting Processes and Administrative Hurdles

The proliferation of charging infrastructure is significantly hampered by cumbersome permitting processes and administrative barriers across various European jurisdictions, which is further hampering the European electric vehicle charger market expansion. Each member state, and often individual municipalities, maintains distinct regulatory requirements for installing charging stations. This fragmentation leads to prolonged approval times and increased operational costs for developers. According to the European Commission, the average time to obtain permits for renewable energy and related infrastructure projects can exceed two years in some regions. Such delays deter investment and slow down the deployment of critical charging networks. In densely populated urban centers, space constraints and zoning laws further complicate the installation process. Local authorities often struggle to balance the need for infrastructure with preservation of historical sites and public spaces. As per a report by ChargeUp Europe, inconsistent regulations regarding grid connection fees and access rights create an uneven playing field for market participants. Small and medium-sized enterprises face particular difficulties navigating these bureaucratic labyrinths, limiting competition and innovation. Moreover, the lack of standardized procedures for street works and civil engineering approvals adds another layer of complexity. Developers must engage with multiple stakeholders, including utility companies, local councils, and environmental agencies, each with their own timelines and requirements. This administrative friction results in inefficiencies that inflate project costs and delay the realization of charging infrastructure goals. Streamlining these processes through harmonizedEU-widee guidelines and digital permitting platforms is essential to accelerate deployment and meet the ambitious targets set by continental climate policies.

MARKET OPPORTUNITIES Integration of Vehicle-to-Grid Technology Solutions

The emergence of vehicle-to-grid technology is a promising opportunity for the Europe electric vehicle charger market. This bidirectional charging capability allows electric vehicles to not only draw power from the grid but also feed stored energy back during peak demand periods. Such functionality turns electric vehicles into mobile energy storage units, enhancing grid stability and facilitating the integration of renewable energy sources. According to the International Energy Agency, smart charging and vehicle-to-grid technology could provide up to 500 gigawatts of flexible capacity globally by 2030 if widely adopted. This potential offers significant economic benefits to both consumers and utility providers. Charge point operators can leverage this technology to offer value-added services such as demand response programs and frequency regulation. As per a study by BloombergNEF, bidirectional charging and smart energy services could generate substantial additional revenue streams annually by optimizing energy trading. The technical standards for vehicle-to-grid interactions are increasingly being harmonized across Europe, fostering interoperability and consumer confidence. Major automakers like Nissan and Volkswagen are already introducing models compatible with bidirectional charging. This technological advancement aligns with the broader goal of creating a smart and resilient energy system. By incentivizing users to participate in grid balancing activities through dynamic pricing models, stakeholders can unlock new business models. The successful implementation of vehicle-to-grid solutions requires collaboration between automakers, charging infrastructure providers, and grid operators to establish robust communication protocols and cybersecurity measures. This synergy promises to redefine the role of electric vehicles in the energy landscape.

Expansion of Ultra-Fast Charging Networks along Corridors

The strategic development of ultra-fast charging networks along major trans-European transport corridors offers a substantial opportunity for market growth. These high-power charging stations, typically exceeding 150 kilowatts, are essential for enabling long-distance travel and reducing journey times for electric vehicle users. The Alternative Fuels Infrastructure Regulation mandates the installation of such facilities at regular intervals, creating a clear roadmap for investment. According to the European Commission, the deployment of a comprehensive ultra-fast charging network is a key priority to address range anxiety for intercity travelers. Energy companies and specialized charging providers are competing to establish dominant positions along these lucrative routes. As per data from Ionity, a joint venture of major automakers, the high utilization rate of high-power charging stations along highways reflects the commercial viability of corridor-based charging infrastructure. Furthermore, the integration of renewable energy sources at these sites enhances their sustainability profile and appeal to environmentally conscious consumers. Solar canopies and onsite battery storage systems are increasingly being incorporated to mitigate grid impact and reduce operational costs. The standardization of payment systems and plug types across borders further facilitates seamless cross-border travel. By focusing on these high-traffic arteries, stakeholders can maximize return on investment while contributing to the broader goal of decarbonizing long-haul transport. This targeted expansion strategy ensures that the charging infrastructure evolves in tandem with the growing capabilities of electric vehicles.

MARKET CHALLENGES Interoperability and Standardization Fragmentation Issues

A persistent challenge facing the Europe electric vehicle charger market is the lack of seamless interoperability and standardization across different networks and providers. Despite efforts to harmonize standards, users often encounter difficulties when using charging stations operated by different entities. Issues such as incompatible payment methods, varying authentication protocols, and inconsistent user interfaces create friction and diminish the overall customer experience. According to a survey by the European Alternative Fuels Observatory, approximately 40% of electric vehicle drivers reported problems with accessing public charging points due to technical or administrative barriers. This fragmentation undermines consumer confidence and hinders the widespread adoption of electric mobility. The proliferation of proprietary software platforms and closed ecosystems further exacerbates the problem. Charge point operators often prioritize brand loyalty over open access, leading to a siloed market structure. As per the European Commission, the implementation of the Open Charge Point Protocol is being promoted to allow users to roam freely between networks. Additionally, the rapid evolution of charging technologies means that older stations may not be compatible with newer vehicle models or communication standards. This technological obsolescence requires continuous upgrades and investments, placing a financial burden on operators. Achieving true interoperability requires concerted efforts from regulators, industry stakeholders, and standardization bodies to enforce common protocols and ensure equitable access. Until these issues are resolved, the full potential of the charging infrastructure will remain unrealized, hindering the seamless integration of electric vehicles into the European transport system.

High Initial Capital Expenditure and Operational Costs

The substantial initial capital expenditure and ongoing operational costs associated with deploying and maintaining charging infrastructure pose a significant challenge to market participants. Installing high-power charging stations requires significant investment in hardware, grid connections, and civil works. According to the International Energy Agency, the cost of installing a single direct current fast charger can range from 15,000 to 150,000 euros, depending on location and power capacity. These high upfront costs deter smaller players and limit the pace of expansion, particularly in less profitable rural areas. Furthermore, operational expenses such as electricity procurement, maintenance, and network management add to the financial burden. As per a report by the European Commission, the utilization rates of many public charging points must reach specific thresholds for operators to achieve profitability in the long term. This economic uncertainty discourages private investment and necessitates government subsidies to bridge the gap. The volatility of electricity prices further complicates financial planning for charge point operators. Fluctuating energy costs can erode margins and make pricing strategies unpredictable for consumers. Additionally, the need for regular software updates and hardware repairs to ensure reliability and security incurs recurring costs. The financial viability of charging infrastructure projects depends heavily on achieving economies of scale and optimizing operational efficiency. Without innovative financing models and supportive policy frameworks, the high cost structure remains a formidable barrier to the widespread deployment of a robust and accessible charging network across Europe.

REPORT COVERAGE

REPORT METRIC

DETAILS

Market Size Available

2025 to 2034

Base Year

2025

Forecast Period

2026 to 2034

CAGR

12.53%

Segments Covered

By Vehicle Type, End User, Charging Type, And Region

Various Analyses Covered

Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities

Regions Covered

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic

Market Leaders Profiled

ABB Ltd., Siemens AG, Schneider Electric SE, Alfen N.V., EVBox Group, ChargePoint Holdings Inc., BP Pulse, Shell Recharge, Ionity GmbH, Tesla Inc.

SEGMENTAL ANALYSIS By Vehicle Type Insights

The battery electric vehicle segment led the market by commanding for 61.6% of the regional market share in 2025. This dominance is primarily driven by the exclusive reliance of BEVs on external charging sources, necessitating a robust and extensive network of public and private chargers. Unlike hybrid variants, BEVs possess no internal combustion engine backup, making charging accessibility a critical determinant of usability. According to the European Automobile Manufacturers Association, battery electric cars represented 14.6% of new car registrations in the European Union in 2023, a figure that continues to rise as model availability expands. The regulatory push towards zero-emission zones in major cities further accelerates BEV adoption, thereby increasing the requirement for dedicated charging points. As per the International Energy Agency, the global stock of battery electric cars reached approximately 30 million in 2023, with Europe representing a substantial portion of this installed base that requires consistent energy replenishment. The average daily driving distance of European commuters, which stands at approximately 40 kilometers, aligns well with the range capabilities of modern BEVs, provided that charging infrastructure is readily available. This synergy between vehicle capability and infrastructure necessity solidifies the leading position of the BEV segment. Furthermore, government incentives such as purchase subsidies and tax exemptions are predominantly targeted at fully electric models, skewing consumer preference towards BEVs and consequently driving the demand for compatible high-power charging solutions across the continent.

On the other hand, the plug-in hybrid electric vehicle segment is another promising segment and is estimated to witness a CAGR of 13.3% over the forecast period, owing to its role as a transitional technology for consumers hesitant to adopt full electrification. This growth is fueled by the flexibility PHEVs offer, allowing users to operate in electric mode for short urban commutes while retaining the security of a gasoline engine for longer journeys. According to the European Automobile Manufacturers Association, plug-in hybrids accounted for 7.7% of new car sales in the EU in 2023, indicating a steady uptake among fleet operators and private buyers seeking reduced emissions without range anxiety. The expansion of workplace charging infrastructure significantly supports this segment, as many employers install alternating current chargers to support employee vehicles. As per a study by the European Alternative Fuels Observatory, a significant portion of PHEV drivers charge their vehicles primarily at work or home, highlighting the importance of accessible Level 2 charging points. The technological advancements in battery capacity for PHEVs, with newer models offering electric ranges exceeding 80 kilometers, further enhance their appeal and charging frequency. This increased electric range necessitates more frequent charging compared to earlier generations, thereby boosting the demand for charging infrastructure. Additionally, corporate fleet regulations in countries like Germany and France encourage the adoption of low-emission vehicles, making PHEVs an attractive option for companies aiming to meet sustainability targets while maintaining operational flexibility.

By End User Insights

The residential segment held the dominant position in the Europe electric vehicle charger market by capturing 54.5% of the regional market share in 2025. The growth of the residential segment in the European market is attributed to the fundamental charging behavior of electric vehicle owners, who prefer the convenience and cost-effectiveness of charging their vehicles overnight at home. According to the European Commission, approximately 80% of all electric vehicle charging events occur at private residences or workplaces, underscoring the critical role of home charging infrastructure. The proliferation ofsingle-familyy homes and apartment complexes with dedicated parking spaces in Northern and Western Europe facilitates the installation of private charging points. As per Eurostat, the homeownership rate in the European Union averages around 69%, providing a stable base for residential charger deployment. Government grants and subsidies specifically targeted at home charger installations further stimulate this segment. For instance, programs in various European countries offer financial incentives covering a portion of the installation costs, making it economically viable for households to invest in private charging solutions. The integration of smart home energy management systems also enhances the appeal of residential chargers, allowing users to optimize charging times based on electricity tariffs. This trend towards decentralized charging reduces the strain on public infrastructure and aligns with consumer preferences for privacy and convenience, solidifying the residential segment’s market leadership.

However, the commercial segment is on the rise and is estimated to exhibit a CAGR of 15.5% over the forecast period, owing to the rapid expansion of public charging networks and corporate fleet electrification initiatives. This surge is propelled by the increasing need for visible and accessible charging infrastructure in urban centers, shopping malls, and highway service stations to supportlong-distancee travel and urban mobility. According to the European Commission, the Alternative Fuels Infrastructure Regulation mandates a significant increase in publicly accessible charging points, compelling commercial entities to invest heavily in infrastructure development. The rise of electric ride-hailing and delivery services further amplifies demand, as these operations require reliable and fast charging solutions to minimize downtime. As per reports from leading mobility platforms, companies aim to become zero-emission platforms in major European cities by 2030, necessitating partnerships with commercial charging providers. Additionally, retail businesses are installing chargers to attract customers and increase dwell time, recognizing the value-added service potential. The deployment of ultra-fast charging hubs by energy companies and specialized operators along major transport corridors also contributes to this growth. These commercial installations often feature higher power outputs and advanced payment systems, catering to a diverse user base and generating substantial revenue streams, thereby attracting significant investment and accelerating market expansion.

By Charging Type Insights

The off-board chargers segment was the leading segment in the Europe electric vehicle charger market and held 59.4% of the regional market share in 2025. This dominance is driven by the superior power delivery capabilities of off-board systems, which enable faster charging times essential for public and commercial applications. Unlike on-board chargers, which are limited by the vehicle’s internal converter capacity, off-board chargers can deliver high power direct current directly to the battery, significantly reducing charging duration. According to the International Energy Agency, the deployment of fast chargers, which are primarily off-board, has seen significant global growth, reflecting the demand for rapid charging solutions. The strategic placement of these chargers along highways and in urban hubs addresses the critical issue of range anxiety, making them indispensable for long-distance travel. As per the European Alternative Fuels Observatory, the number of direct current charging points in the European Union exceeded 100,000 in 2023, highlighting the extensive rollout of off-board infrastructure. The technological advancement in power electronics has also reduced the cost and size of off-board chargers, making them more accessible for widespread deployment. Furthermore, the compatibility of off-board chargers with a wide range of vehicle models ensures their relevance in a heterogeneous market. The ability to support future battery technologies with higher charging acceptance rates further cements the leading position of off-board chargers in the evolving landscape of electric mobility infrastructure.

On the other side, the on-board chargers segment is experiencing robust growth and is estimated to record a CAGR of 10.2% over the forecast period, owing to the increasing integration of advanced charging capabilities within electric vehicles themselves. While off-board chargers dominate public infrastructure, the reliance on on-board chargers for alternating current charging at home and workplaces remains significant. This growth is fueled by the rising sales of plug-in hybrid and entry-level battery electric vehicles, which typically utilize slower alternating current charging methods for daily needs. According to the European Automobile Manufacturers Association, the majority of electric vehicles sold in Europe are equipped with on-board chargers, catering to overnight charging requirements. The improvement in efficiency and reduction in weight of on-board charging units have made them more attractive to automakers seeking to optimize vehicle performance and range. As per technological reports, the market for on-board chargers is expanding due to the adoption of bidirectional charging technologies, which allow vehicles to supply power back to the grid or home. This functionality adds value to the on-board charger, transforming it from a simple component into a key element of vehicle-to-grid systems. The standardization of charging protocols and the increasing prevalence of smart charging features within vehicles further support the growth of this segment, which is ensuring its continued relevance in the overall charging ecosystem.

REGIONAL ANALYSIS Germany Electric Vehicle Charges Market Analysis

Germany was the largest national market for electric vehicle chargers in Europe and accounted for 23.6% of the regional market share in 2025. The leading position of Germany in the European market is mainly attributed to its strong automotive industry and ambitious climate targets, which drive substantial investment in charging infrastructure. According to the Federal Network Agency, Germany had over 120,000 public charging points by the end of 2023, reflecting a concerted effort to support the growing electric vehicle fleet. The German government’s Masterplan Charging Infrastructure II outlines plans to install one million public charging points by 2030, providing a clear roadmap for market expansion. This initiative is supported by significant funding programs that incentivize the deployment of fast charging stations along federal highways and in urban areas. As per the Federal Motor Transport Authority, new electric vehicle registrations in Germany reached approximately 524,000 in 2023, creating a robust demand for reliable charging solutions. The presence of major automakers such as Volkswagen and BMW further accelerates infrastructure development through proprietary networks and partnerships. Additionally, the integration of renewable energy sources into the charging grid aligns with Germany’s Energiewende policy, enhancing the sustainability profile of the market. The combination of regulatory support, industrial strength, and consumer adoption positions Germany as the pivotal hub for electric mobility infrastructure in Europe.

France Electric Vehicle Charges Market Analysis

France had the second-largest share of the European electric vehicle charger market in 2025. The French market is characterized by strong government intervention and a focus on equitable access to charging infrastructure across urban and rural regions. According to the French Ministry for the Ecological Transition, the number of public charging points in France exceeded 110,000 in 2023, supported by the Advenir program, which provides subsidies for installation. The French government has mandated the installation of charging points in new residential and commercial buildings, ensuring that infrastructure growth keeps pace with vehicle adoption. As per the European Alternative Fuels Observatory, France has one of the most comprehensive networks of charging points in Europe, catering to the diverse needs of its electric vehicle users. The country’s commitment to phasing out internal combustion engine vehicles by 2035 further stimulates market growth. Major energy companies are actively expanding their charging networks, leveraging their existing retail presence to deploy chargers at service stations and supermarkets. The emphasis on interoperability and user-friendly payment systems enhances the customer experience, encouraging wider adoption. France’s strategic approach combines regulatory mandates with financial incentives, creating a conducive environment for sustained market expansion.

United Kingdom Electric Vehicle Charges Market Analysis

The United Kingdom is estimated to account for a promising share of the European electric vehicle charger market during the forecast period. The UK market is distinguished by its advanced regulatory framework and high level of private sector investment in charging infrastructure. According to the Department for Transport, the UK had over 53,000 public charging devices by early 2024, with a significant proportion being rapid chargers. The government’s Zero Emission Vehicle Mandate requires an increasing percentage of new car sales to be zero emission, driving demand for supporting infrastructure. As per Zap Map data, the number of public chargers in the UK has increased by 45% year on year, indicating growing consumer confidence. The UK’s approach emphasizes competition and innovation, with numerous private operators deploying diverse charging solutions. The introduction of the Public Charge Point Regulations ensures reliability and transparency in pricing, addressing previous consumer concerns. The geographic distribution of chargers is improving, with targeted investments in underserved areas to ensure nationwide coverage. The strong presence of companies facilitating seamless payment experiences further enhances the market appeal. The UK’s proactive policy environment and dynamic private sector collaboration position it as a key driver of electric mobility infrastructure development in Europe.

Netherlands Electric Vehicle Charges Market Analysis

The Netherlands is expected to showcase a healthy CAGR in the European electric vehicle charger market over the forecast period. The Netherlands is renowned for having the highest density of charging points per capita in Europe. The country’s market is defined by its early adoption of electric mobility and comprehensive urban planning strategies. By the end of 2025, the Netherlands significantly surpassed its earlier milestones, reaching a total of 209,513 charging points. This network includes approximately 126,058 regular public chargers and over 6,500 fast-charging points (above 50 kW). The Dutch government has implemented strict emissions zones in major cities like Amsterdam and Rotterdam, compelling residents and businesses to switch to electric vehicles. As per the International Council on Clean Transportation, the Netherlands has maintained a benchmark ratio of approximately one public charging point for every ten electric vehicles. The collaborative model involving municipalities, housing corporations, and private operators has been instrumental in this success. Furthermore, the focus on smart charging and vehicle-to-grid (V2G) integration is particularly advanced, leveraging the country’s robust digital infrastructure. The widespread availability of charging points in residential areas alleviates range anxiety and supports a new passenger car market where BEVs and PHEVs together accounted for nearly 49% of registrations in 2025.

Italy Electric Vehicle Charges Market Analysis

Italy is predicted to grow at a notable CAGR in the European electric vehicle charger market over the forecast period due to its rapidly accelerating adoption rate, driven by the National Recovery and Resilience Plan (PNRR). As of early 2026, the number of public charging points in Italy has seen a significant surge; for instance, Enel alone recently completed the installation of over 3,700 new charging stations under the first PNRR tender, with 40% of these located in southern Italy. The National Recovery and Resilience Plan has earmarked billions to support e-mobility, aiming to install thousands of high-power stations to bridge the historical gap with Northern European economies. In November 2025, Italy’s BEV market share saw a record leap to 12.2%, spurred by targeted government purchase incentives. The geographical challenge of connecting the north and south has been met with a strategic corridor charging along major highways, providing power outputs of up to 90 kW per connection at new sites. Energy companies like Enel X are playing a pivotal role in deploying these smart solutions and integrating renewable energy. Italy’s market is currently in a phase of high-velocity growth as infrastructure gaps are filled and policy support—such as the PNRR revisions expected in 2026—continues to strengthen its position in the European landscape.

COMPETITION OVERVIEW

The competition in the Europe electric vehicle charger market is intense and characterized by a diverse mix of established industrial giants, specialized charging network operators, and emerging technology startups. Major electrical equipment manufacturers leverage their global supply chains and engineering prowess to dominate the hardware segment. Simultaneously, dedicated charging service providers focus on building extensive networks and enhancing user experience through digital platforms. The market sees frequent strategic alliances between automakers and energy companies to create integrated ecosystems. Regulatory pressures and standardization efforts further shape competitive dynamics by enforcing interoperability requirements. Price competition remains fierce, particularly in the residential segment, where cost sensitivity is high. Innovation in ultra-fast charging technology serves as a key differentiator for players targeting commercial and public infrastructure segments. The entry of new competitors from Asia adds pressure on European firms to maintain technological leadership. Overall, the landscape is dynamic with continuous shifts in market positioning driven by technological advancements and policy changes.

KEY MARKET PLAYERS

A few major players of the Europe electric charger market include

ABB Ltd Siemens AG Schneider Electric SE Alfen N.V EVBox Group ChargePoint Holdings Inc BP Pulse Shell Recharge Ionity GmbH Tesla Inc Top Strategies Used by Key Market Participants

Key players in the Europe electric vehicle charger market primarily employ strategic partnerships and collaborations to expand their network reach and enhance technological capabilities. Companies frequently join forces with automotive manufacturers, energy utilities, and retail chains to deploy charging stations at high-traffic locations. Another prevalent strategy involves significant investment in research and development to innovate faster and more efficient charging technologies. Firms focus on developing ultra-fast chargers and smart charging solutions that integrate with renewable energy sources. Geographic expansion is also critical, with companies targeting underserved regions to capture emerging opportunities. Additionally, mergers and acquisitions allow larger entities to consolidate market presence and acquire specialized technologies. Providing comprehensive service packages, including installation, maintenance, and software management, helps differentiate offerings. These strategies collectively drive growth and competitiveness in the rapidly evolving landscape of electric mobility infrastructure across the European continent.

Leading Players in the Market ABB Ltd stands as a pivotal force in the Europe electric vehicle charger market by delivering comprehensive high-power charging solutions. The company leverages its extensive global engineering expertise to manufacture robust direct current fast chargers that support rapid energy transfer. ABB recently expanded its Terra High Power Charging portfolio to meet the growing demand for ultra-fast infrastructure along major European transport corridors. Their strategic partnerships with automotive manufacturers and energy providers facilitate seamless integration of charging networks. By focusing on interoperability and reliability, ABB ensures that its technology supports diverse vehicle models. The company continues to invest in research and development to enhance charger efficiency and reduce operational costs. This commitment to innovation strengthens their position as a preferred supplier for large-scale infrastructure projects across the continent. Siemens AG contributes significantly to the Europe electric vehicle charger market through its advanced digitalization and electrification technologies. The company offers a wide range of alternating current and direct current charging solutions tailored for residential, commercial, and public applications. Siemens recently launched enhanced versions of its VersiCharge series, incorporating smart connectivity features that enable remote monitoring and management. Their focus on integrating renewable energy sources with charging infrastructure supports sustainable mobility goals. Siemens collaborates with utility companies to develop grid-friendly charging solutions that optimize energy consumption. By leveraging its strong industrial base and digital platforms, Siemens provides scalable and efficient charging systems. This approach helps cities and businesses deploy reliable infrastructure while managing grid stability effectively. Schneider Electric SE plays a crucial role in the Europe electric vehicle charger market by providing energy management and automation solutions. The company offers a comprehensive suite of EV charging products, including wall boxes and public charging stations designed for optimal performance. Schneider Electric recently expanded its EVlink portfolio with new models featuring improved user interfaces and enhanced safety protocols. Their emphasis on sustainability drives the integration of solar power and battery storage with charging infrastructure. The company actively partners with property developers and facility managers to install smart charging systems in buildings. By focusing on energy efficiency and digital services, Schneider Electric enables users to monitor and control charging processes remotely. This strategy supports the transition to low-carbon mobility while ensuring reliable and convenient charging experiences for consumers across Europe. MARKET SEGMENTATION

This research report on the Europe electric vehicle charger market has been segmented and sub-segmented based on Vehicle Type, End User, Charging Type & region.

By Vehicle Type

Battery Electric Vehicle (BEV) Plug-in Hybrid Electric Vehicle (PHEV) Hybrid Electric Vehicle (HEV)

By End User

By Charging Type

On-board Chargers Off-board Chargers

By Region

UK France Spain Germany Italy Russia Sweden Denmark Switzerland Netherlands Turkey Czech Republic Rest of Europe