Valuation Check As UK Ofgem Approval Opens New Energy Market Opportunity")

Tesla (TSLA) has just secured regulatory approval from UK energy watchdog Ofgem to supply electricity to homes and businesses, marking a clear push into retail power alongside its renewable generation and storage offerings.

See our latest analysis for Tesla.

Against that backdrop, Tesla’s recent share price performance has cooled, with a 30 day share price return of 8.66% and a 90 day return of 14.76%, even as its 1 year total shareholder return of 56.49% and 3 year total shareholder return of 117.18% reflect how strong the longer term run has been. The Ofgem approval, alongside moves into AI projects and energy storage, is landing at a time when some investors are reassessing growth expectations and risk around EV demand and new capital intensive ventures.

If this energy pivot has your attention, it may be a useful time to review what other companies are building the infrastructure behind electrification and grid upgrades, starting with 23 power grid technology and infrastructure stocks.

With Tesla shares up 56.49% over the past year yet down over the last 30 and 90 days, and trading only about 8% below the average analyst price target, you have to ask yourself: is there still a buying opportunity here, or is the market already pricing in the next phase of growth?

Most Popular Narrative: 33.5% Undervalued

At $391.20, Tesla trades below the $588.18 fair value put forward in the most followed narrative, which leans heavily on AI, autonomy and robotics to justify that gap.

Tesla is not just an automaker, it is in the process of evolving into a technology company spanning AI, robotics, and mobility services. This transformation, much like Nvidia’s shift from GPUs to AI computing, is unlocking new revenue streams that could redefine Tesla’s valuation.

Want to see what sits behind that bold price tag? This narrative leans on rapid revenue expansion, rising margins and a premium future earnings multiple. Curious which numbers have to line up to support a tech style valuation on an auto heavy business model?

Result: Fair Value of $588.18 (UNDERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, this story still hinges on Tesla executing complex AI and robotaxi plans while managing regulatory approvals and heavy capital spending, any of which could sharply reset expectations.

Find out about the key risks to this Tesla narrative.

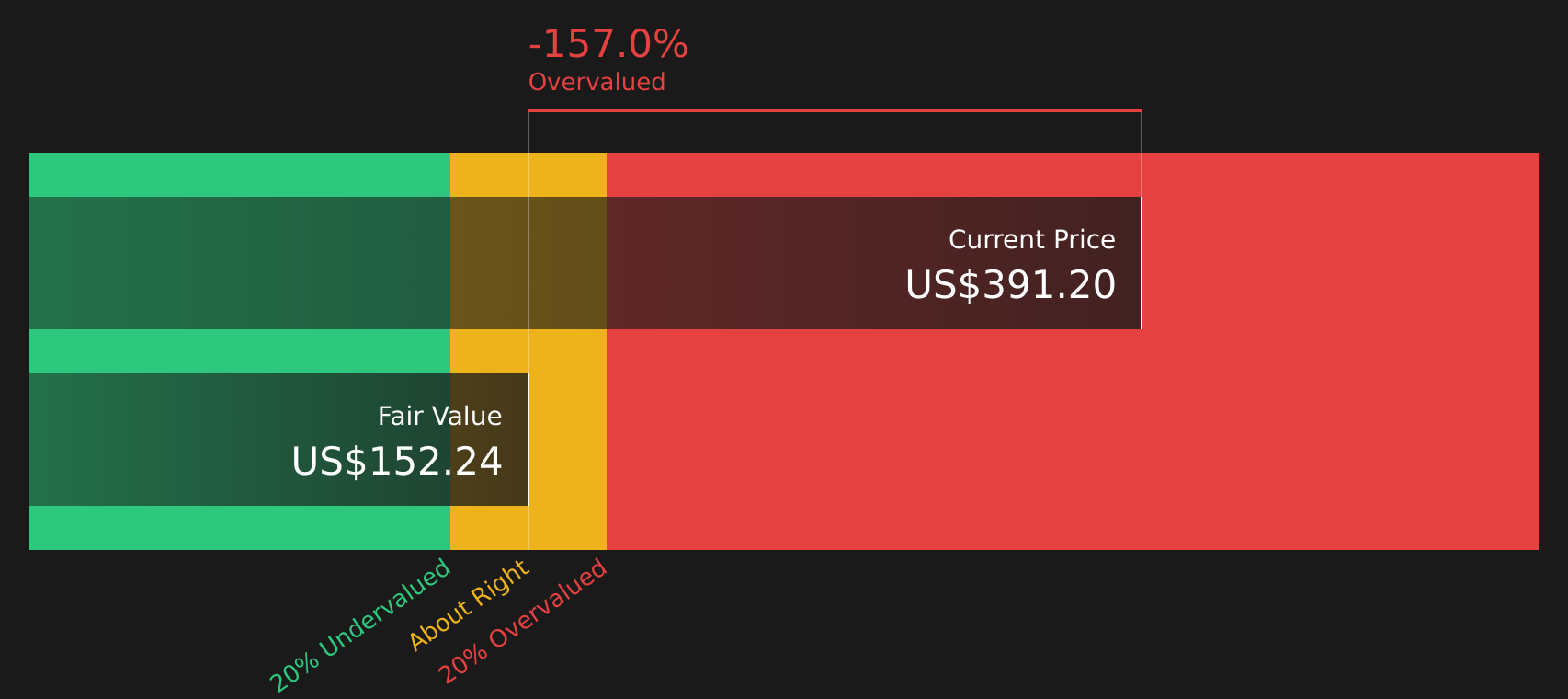

Another View: Cash Flows Paint a Harsher Picture

That 33.5% undervaluation from the narrative is only one lens. Our DCF model, which looks at Tesla’s future cash flows, points the other way, with a fair value of $152.24 against a $391.20 share price. This implies the stock is overvalued. Which story do you trust more?

Look into how the SWS DCF model arrives at its fair value.

TSLA Discounted Cash Flow as at Mar 2026Next Steps

TSLA Discounted Cash Flow as at Mar 2026Next Steps

With such mixed signals on value and future potential, it makes sense to move quickly and test the assumptions yourself using 1 key reward and 2 important warning signs.

Looking for more investment ideas?

If this Tesla story has you thinking bigger about your portfolio, do not stop here. The right list of ideas could be exactly what you are missing.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we’re here to simplify it.

Discover if Tesla might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com