Tesla (NasdaqGS:TSLA) is shifting its core focus from premium electric vehicles to robotics, artificial intelligence, and autonomous systems. The company is discontinuing the Model S and Model X and converting parts of its manufacturing footprint to produce the Optimus humanoid robot. Tesla is launching its Cybercab autonomous vehicle and restructuring Full Self Driving into a subscription based service. The robotaxi pilot is being scaled while the company addresses technical issues, regulatory scrutiny, and recent collisions involving its autonomous fleet. Tesla is planning higher capital expenditures to support these new initiatives and a broader move away from a maturing, highly competitive EV market.

For you as an investor, Tesla is no longer just an electric car manufacturer; it is positioning itself as a robotics and AI platform company built around autonomy. This pivot touches every part of the business, from product mix and factory use to software monetization and regulatory exposure. The changes matter because they affect how Tesla (NasdaqGS:TSLA) earns revenue, allocates capital, and competes with both automakers and technology firms.

Looking ahead, the key questions are less about individual vehicle models and more about adoption and regulation of robotaxis, traction for Optimus in real world use cases, and uptake of subscription based Full Self Driving. Your assessment will likely hinge on how you weigh the execution and safety risks of this shift against the potential scale of these new business lines and the capital required to build them out.

Stay updated on the most important news stories for Tesla by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on Tesla.

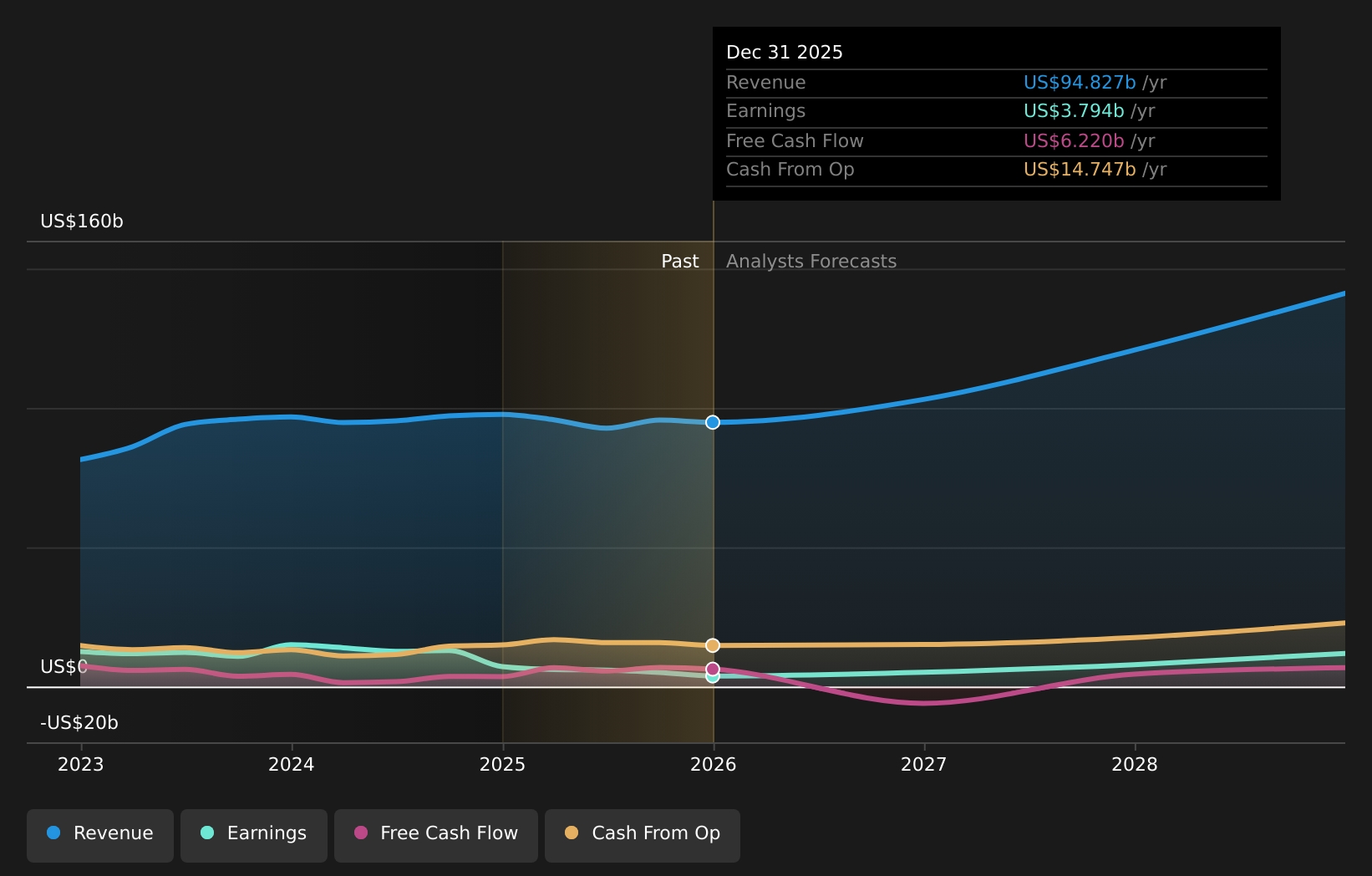

NasdaqGS:TSLA Earnings & Revenue Growth as at Feb 2026

NasdaqGS:TSLA Earnings & Revenue Growth as at Feb 2026

1 thing going right for Tesla that this headline doesn’t cover.

This pivot effectively turns Tesla into a capital intensive AI and robotics platform tied to its existing EV and energy base. Discontinuing the higher priced Model S and Model X frees factory capacity and management focus for Optimus and Cybercab, but it also leans harder on a still challenged core auto business where 2025 revenue declined and competition from players like BYD and Xiaomi has intensified. Shifting Full Self Driving to a subscription model and scaling robotaxis aim to increase software like recurring revenue, yet those ambitions now sit alongside higher regulatory scrutiny and legal overhangs from Autopilot related crashes.

How This Fits Into The Tesla Narrative The move toward robotaxis, Optimus and FSD subscriptions supports the narrative that Tesla is pushing for higher margin, recurring revenue streams from autonomy and physical AI rather than relying only on vehicle sales. The need for heavy capex, slower product ramps and regulatory friction around autonomy challenges the idea that these new businesses will translate smoothly into stronger margins and earnings in the near term. The explicit factory conversion to Optimus and the refocus away from premium models add execution and capital allocation choices that are not fully captured in the existing long term growth story.

Knowing what a company is worth starts with understanding its story.

Check out one of the top narratives in the Simply Wall St Community for Tesla to help decide what it’s worth to you.

The Risks and Rewards Investors Should Consider ⚠️ Heavy spending on factories, AI infrastructure and robotics could pressure free cash flow if revenue from robotaxis and Optimus takes longer to materialize. ⚠️ Regulatory and safety setbacks around FSD and robotaxis, including reported collisions and lawsuit outcomes, may slow deployment or increase compliance costs compared with competitors like Waymo and Cruise. 🎁 A successful rollout of FSD subscriptions and autonomous ride hailing could increase the share of recurring, software like revenue tied to Tesla’s installed vehicle base. 🎁 If Optimus and Cybercab gain traction, Tesla could diversify away from a maturing EV market and build new revenue streams that are less sensitive to traditional auto cycles and pricing pressure from BYD or legacy automakers. What To Watch Going Forward

You will want to watch the pace of FSD subscription uptake, safety metrics and regulatory approvals for robotaxis across new cities, not just headline product launches. Factory conversion for Optimus and Cybercab is another key test, because delays or cost overruns could weigh on margins while Tesla’s core EV business is already under pressure from price cuts and competition. Tracking how quickly the company turns high capex in AI compute, batteries and robotics into measurable revenue and profit contribution will be central to judging whether this new focus is adding shareholder value or stretching the balance sheet.

To ensure you’re always in the loop on how the latest news impacts the investment narrative for Tesla, head to the

community page for Tesla to never miss an update on the top community narratives.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we’re here to simplify it.

Discover if Tesla might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

")