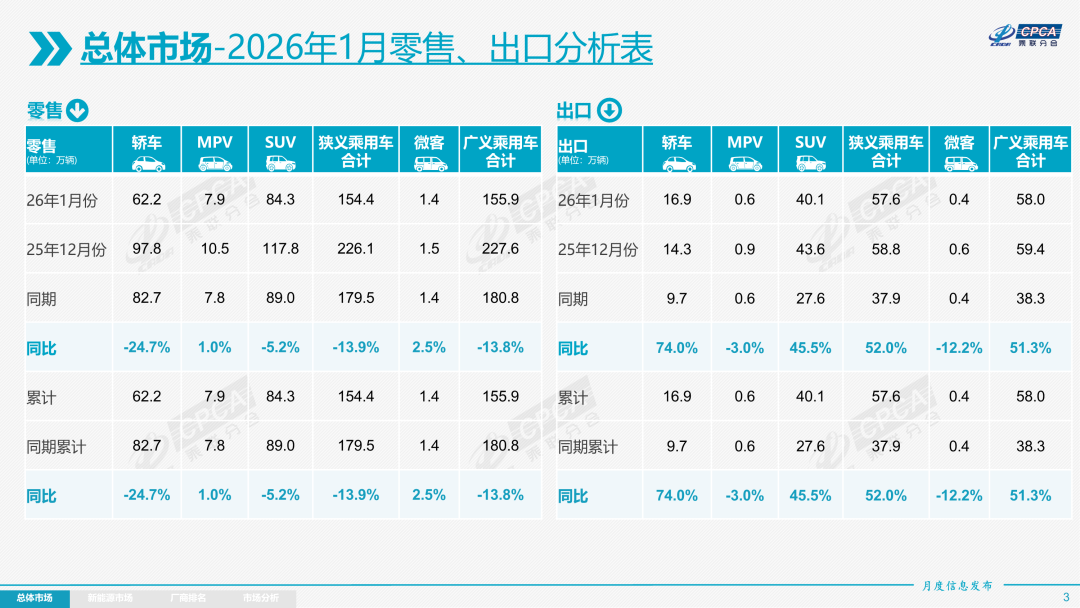

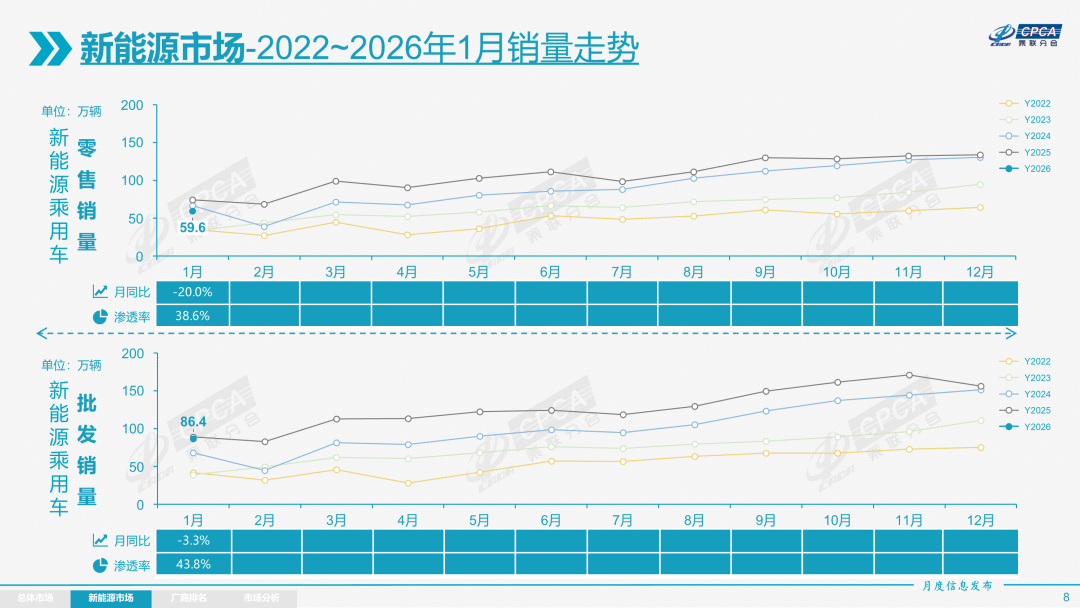

According to Zhitong Finance APP, data from the Passenger Car Association shows that in January, retail sales of the national passenger car market reached 1.544 million units, a year-on-year decrease of 13.9%. Retail sales of new energy passenger cars reached 596,000 units, with a retail penetration rate of new energy vehicles in the overall domestic passenger car market at 38.6%, down by 3 percentage points compared to the same period last year.

In terms of exports, in January, passenger car exports (including complete vehicles and CKD) reached 576,000 units, a year-on-year increase of 52.0%. New energy vehicles accounted for 49.6% of total exports in January, an increase of 13 percentage points over the same period. Exports of self-owned brands reached 476,000 units, up 49% year-on-year; joint venture and luxury brand exports were 100,000 units, growing 65% year-on-year.

January National Passenger Car Market Review

January National Passenger Car Market Review

In January 2026, self-owned brand fuel passenger car exports reached 250,000 units, up 17% year-on-year. Self-owned new energy vehicle exports totaled 226,000 units, increasing 115% year-on-year. New energy vehicles accounted for 47.5% of self-owned brand exports, especially with high growth in new energy exports in Europe, Southeast Asia, and other regions, marking the expanding influence of Chinese new energy vehicle brands in the international market and laying a solid foundation for future export growth.

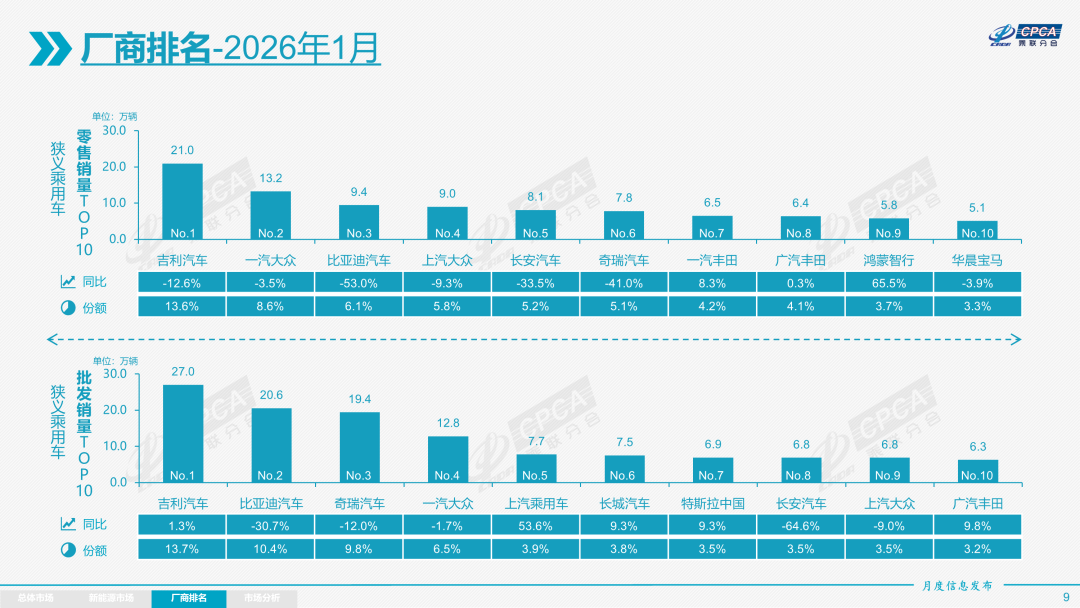

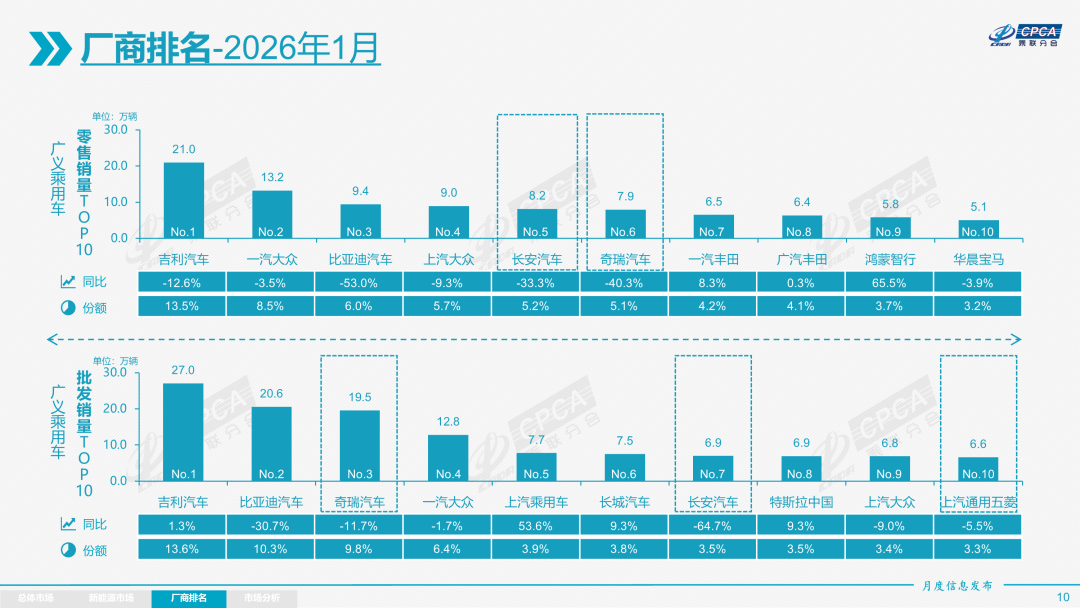

In January, retail sales of self-owned brands reached 890,000 units, down 18% year-on-year. The domestic retail share of self-owned brands was 57.5% for the month, a year-on-year decrease of 3.5 percentage points. Self-owned brands gained significant incremental growth in both the new energy market and the export market. Traditional leading automakers performed exceptionally well in transformation and upgrading, with notable market share increases for traditional automaker brands such as Geely Auto, Changan Automobile, and Great Wall Motors.

Retail sales of mainstream joint venture brands in January reached 470,000 units, down 4% year-on-year. The retail share of German brands was 19.8% in January, up 1.4 percentage points year-on-year, while Japanese brands held a 15.5% retail share, increasing 2.1 percentage points year-on-year. The retail share of American brands stood at 5%, down 0.3 percentage points year-on-year. Korean brands and other Western European brands saw slight increases in their retail shares.

In January, luxury car retail sales reached 180,000 units, a year-on-year decline of 15%. The retail share of luxury brands was 11.6% in January, down 0.5 percentage points year-on-year, with the traditional luxury car market facing greater pressure than the joint ventures.

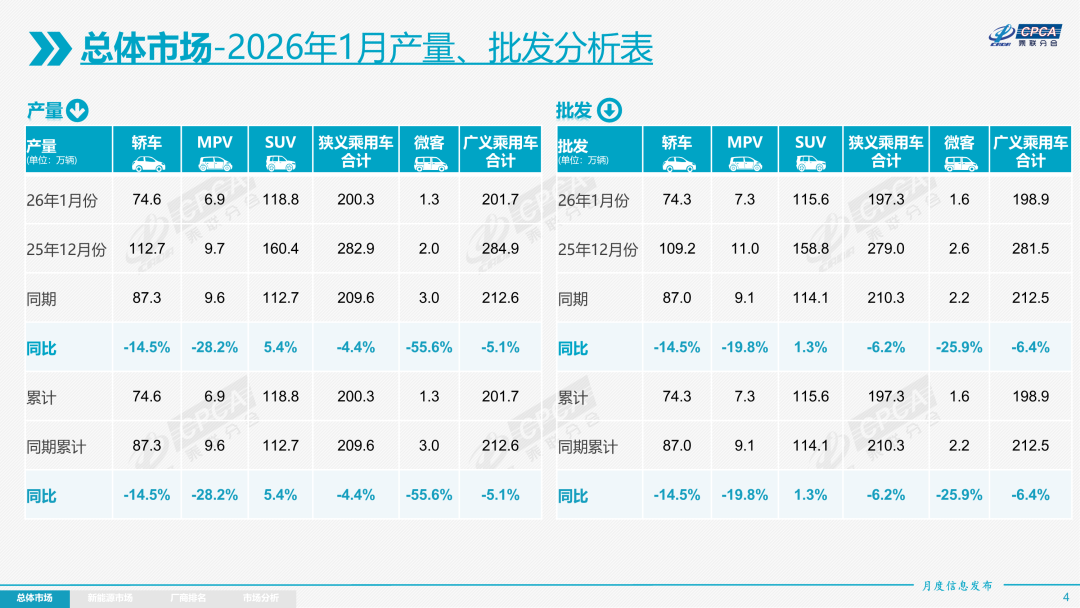

Production: In January, production of passenger cars reached 2.003 million units, down 4.4% year-on-year. Production of luxury brands grew 15% year-on-year; joint venture brands saw a 15% decline in production; production of self-owned brands fell 4% year-on-year.

Wholesale: In January, wholesale volumes from national passenger car manufacturers reached 1.973 million units, down 6.2% year-on-year. Affected by retail adjustments, the year-on-year growth rate of passenger car wholesale in January was 7.7 percentage points higher than the retail growth rate. Wholesale volumes of self-owned automakers reached 1.326 million units, down 8% year-on-year. Mainstream joint venture automakers’ wholesale volumes were 420,000 units, down 4% year-on-year. Luxury car wholesale volumes reached 228,000 units, up 4% year-on-year.

The overall wholesale structure of major passenger car manufacturers continued to change in January, with some mid-tier companies showing signs of gradual rise. SAIC-GM-Wuling, Seres Auto, Xiaomi Auto, and Nio demonstrated relatively strong month-on-month performance. There were four passenger car manufacturers with sales exceeding 100,000 units in January (six in December and five in the same period last year), accounting for 40% of the overall market share (46% last month and 54% during the same period). Manufacturers with wholesale volumes of 50,000-100,000 units accounted for 24% of the market share (28% last month and 18% during the same period), while those with 10,000-50,000 units accounted for 31% of the market share (24% last month and 27% during the same period).

Inventory: Due to stable production by manufacturers in January, wholesale volumes from manufacturers were 31,000 units lower than production. Monthly domestic wholesale was 150,000 units below retail sales. Overall passenger vehicle industry inventory decreased by 110,000 units in January (compared to an 80,000-unit reduction in the same period last year). This January saw involuntary destocking by automakers, whereas last year’s decline was driven by retail demand.

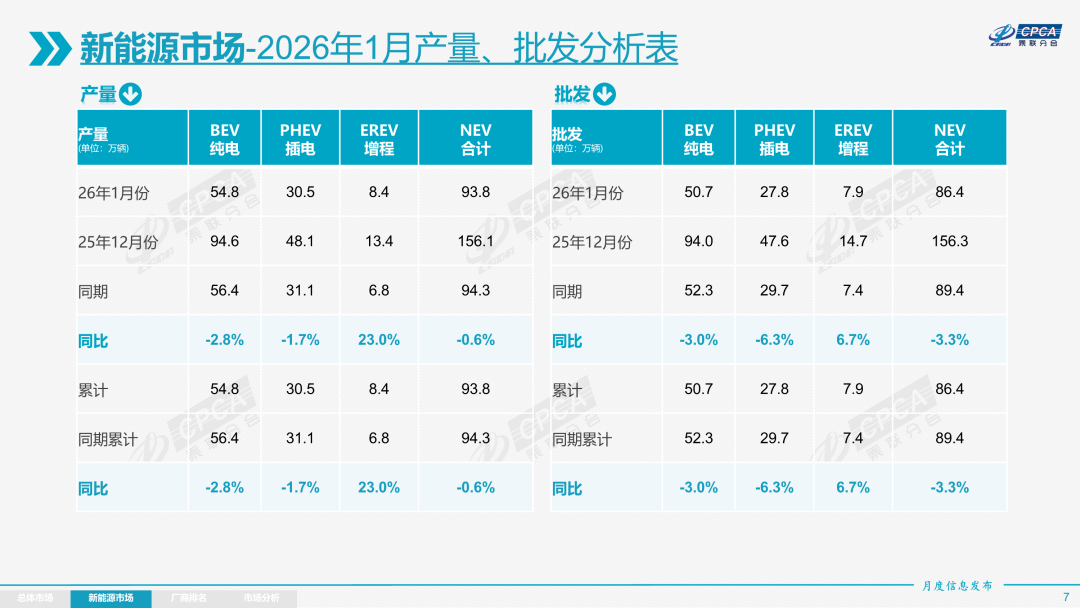

New Energy: Production of new energy passenger vehicles reached 938,000 units in January, representing a year-on-year decrease of 0.6%.

Wholesale sales of new energy passenger vehicles reached 864,000 units in January, a year-on-year decrease of 3.3%; wholesale sales of conventional fuel passenger vehicles amounted to 1.109 million units, marking a year-on-year decline of 9%.

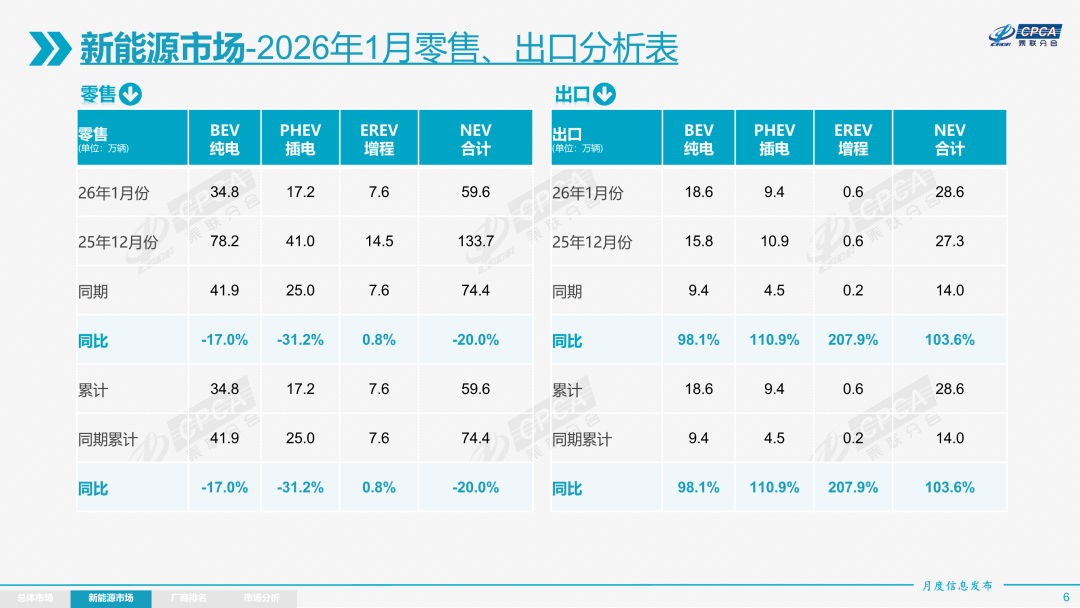

Retail sales of new energy passenger vehicles in the domestic market reached 596,000 units in January, down 20.0% year-on-year; retail sales of conventional fuel passenger vehicles totaled 948,000 units, reflecting a year-on-year drop of 10%.

In January, exports of new energy passenger vehicles by manufacturers reached 286,000 units, a year-on-year increase of 103.6%; exports of conventional fuel passenger vehicles amounted to 290,000 units, up 20% year-on-year.

1) Wholesale: The penetration rate of new energy vehicles (NEVs) in wholesale reached 43.8% in January, an increase of 1.3 percentage points compared to January 2025. The NEV penetration rate for independent brands was 57.9%; for luxury cars, it was 39.8%; while the NEV penetration rate for mainstream joint venture brands was only 3.6%.

Wholesale sales of pure electric vehicles (BEVs) reached 507,000 units in January, marking a year-on-year decline of 3.0%; narrow plug-in hybrid (PHEV) sales totaled 278,000 units, down 6.3% year-on-year; extended-range electric vehicle (EREV) wholesale sales reached 79,000 units, growing 6.7% year-on-year. In January’s NEV wholesale mix: BEVs accounted for 58.3% (a year-on-year decrease of 0.2%), narrow PHEVs made up 32.6% (a year-on-year decrease of 0.6%), and EREVs represented 9.1% (a year-on-year increase of 0.8%).

Wholesale of B-segment electric vehicles (EVs) reached 199,000 units in January, growing 15% year-on-year, accounting for 39% of the BEV market, an increase of 5.9 percentage points compared to the same period last year. The A00+A0 segment of the BEV market faced significant pressure, with A00-class wholesale sales totaling 46,000 units, down 62% year-on-year, representing 9% of the BEV share—a decline of 14.1 percentage points year-on-year. A0-class wholesale sales reached 142,000 units, capturing 28% of the BEV share, up 6.5 percentage points year-on-year; A-class EVs totaled 92,000 units, holding an 18% share, down 2.5 percentage points year-on-year. Growth in affordable EVs is sustainable, as the widespread adoption of such models is key to driving incremental growth in the auto market.

In January, 17 models exceeded 20,000 units in passenger vehicle wholesale sales (compared to 27 models the previous month): BYD Song (42,227 units), Geely Xingyuan (41,676 units), Boyue (41,296 units), Model Y (38,916 units), Xiaomi YU7 (37,869 units), Sagitar (31,303 units), Model 3 (30,213 units), Sylphy (25,953 units), Xingyue L (25,066 units), Wentai M7 (24,977 units), Tan Suo 06 (23,101 units), Lavida (22,878 units), Emgrand (22,826 units), Tiggo 8 (22,626 units), MG ZS (22,148 units), Seagull (20,145 units), and Xingrui (20,024 units). Among these, 13 were NEV models, while recent strong performers among conventional fuel vehicles included Boyue, Sylphy, Sagitar, Lavida, and Tiggo 8.

2) Retail: The retail penetration rate of NEVs in the overall passenger vehicle market was 38.6% in January, a decrease of 3 percentage points compared to the same period last year. In January’s domestic retail, the NEV penetration rate within independent brands was 61.7%; for luxury cars, it was 16.1%; while the NEV penetration rate for mainstream joint venture brands stood at only 4.3%. From the perspective of monthly NEV domestic retail shares, independent brands held 60.1% in January, down 12 percentage points year-on-year; mainstream joint venture brands accounted for 3.9%, up 2 percentage points year-on-year; new forces captured 31.2%, with brands like XPeng Motors (09868), Leapmotor (09863), and Xiaomi Auto (01810) driving a 10-percentage-point increase in their share year-on-year; Tesla’s share was 3.1%, down 1.5 percentage points year-on-year.

3) Exports: In January, new energy passenger vehicle exports reached 286,000 units, a year-on-year increase of 103.6%. They accounted for 49.6% of total passenger vehicle exports, up 12.5 percentage points from the same period last year. Of these, pure electric vehicles accounted for 65% of new energy exports (compared to 67% in the same period last year), with A00+A0 class pure electric vehicles, as the core focus, representing 50% of pure electric exports (up from 41% last year). An increasing number of new energy brand products manufactured in China are going global, gaining rising recognition overseas. Plug-in hybrid vehicles accounted for 33% of new energy exports (32% last year). Despite some recent external interference, independent plug-in hybrid exports to developing countries have grown significantly, showing promising prospects.

In January, companies excelling in new energy exports included BYD (96,859 units), Tesla China (50,644 units), Geely Auto (32,117 units), Chery Automobile (27,033 units), Leapmotor (14,523 units), SAIC Passenger Vehicle (13,071 units), SAIC-GM-Wuling (11,097 units), Dongfeng Motor (6,745 units), Great Wall Motor (6,102 units), Changan Automobile (4,952 units), Beam Auto (3,713 units), Changan Mazda (3,391 units), Volvo Asia Pacific (3,316 units), XPeng Motors (3,204 units), Polestar (2,758 units), Seres Auto (Hubei) (2,108 units), Smartmore Auto (1,665 units), Beijing Automobile Manufacturing Plant (1,530 units), IM Motors (1,250 units), GAC Aion (1,220 units), JAC Motors (833 units), Beijing Hyundai (550 units), and GAC Trumpchi (543 units). Other automakers also achieved notable new energy export volumes.

In terms of overseas system construction, CKD exports account for a significant share among some independent brands. SAIC-GM-Wuling’s CKD exports represent 40.4%, SAIC Passenger Vehicle’s CKD exports account for 1.2%, and Beijing Hyundai’s CKD exports make up 10.4%. Overseas production of fuel vehicles is estimated at over 500,000 units. Adding KD exports of new energy vehicles, Chinese automobile overseas sales are projected to exceed 9 million units.

4) Automakers: In January, new energy passenger vehicle manufacturers showed strong overall performance. BYD’s dual-drive strategy in pure electric and plug-in hybrids solidified its leadership in independent new energy brands. Narrowly defined plug-in hybrids, represented by BYD, Geely Auto, and Chery Automobile, continued to perform strongly. In terms of product deployment, the implementation of independent automakers’ multi-pronged strategy in the new energy sector has steadily expanded the market base. The number of manufacturers achieving monthly wholesale sales exceeding 10,000 units reached 16 (two more than the same period last year), accounting for 90.3% of total new energy passenger vehicles (93% last month, 91.7% last year).

Among them, BYD (205,518 units), Geely Auto (124,252 units), Tesla China (69,129 units), Chery Automobile (46,802 units), Seres Auto (40,200 units), Xiaomi Auto (39,002 units), Leapmotor (32,059 units), SAIC Passenger Vehicle (28,179 units), Li Auto (27,668 units), SAIC-GM-Wuling (27,625 units), Dongfeng Motor (27,431 units), Nio (27,182 units), Changan Automobile (26,974 units), GAC Aion (21,635 units), XPeng Motors (20,011 units), and Great Wall Motor (18,019 units).

Domestic new energy passenger vehicle retail exceeding 20,000 units was achieved by BYD (94,176 units), Geely Auto (92,135 units), HarmonyOS Intelligent Travel (57,915 units), Xiaomi Auto (39,002 units), Changan Automobile (31,122 units), Li Auto (27,668 units), Nio (27,061 units), Dongfeng Motor (22,035 units), GAC Aion (21,297 units), and SAIC-GM-Wuling (20,996 units).

5) New Forces: In January, new forces accounted for 31.2% of retail market share, an increase of 10 percentage points year-on-year. Pure electric vehicle sales within the new forces accounted for 73.8% of their total sales, a substantial rise from 62.1% during the same period last year. Sales of pure electric vehicles in the RMB 100,000-150,000 price range grew significantly. Independent traditional automakers’ independently operated new energy brands, as second-generation innovators, performed strongly, capturing a 18.4% market share, up six percentage points year-on-year. Self-developed new energy brands under major domestic groups like Deep Blue Auto, Yipai Technology, Zeekr, Alpha Fox, and Voyah demonstrated excellent performance.

6) Conventional Hybrids: In January, wholesale sales of conventional hybrid passenger vehicles reached 74,000 units, a year-on-year increase of 0.2%. Among them, GAC Toyota (39,382 units), FAW Toyota (25,963 units), Dongfeng Motor (3,637 units), Changan Ford (2,764 units), Dongfeng Honda (1,920 units), GAC Honda (190 units), GAC Trumpchi (88 units), Geely Auto (73 units), FAW Hongqi (7 units), and Jiangsu Yueda Kia (1 unit). The hybrid market remained relatively stable, with strong overseas performance of independent hybrid models.

Outlook for China’s Passenger Vehicle Market in February

February has 16 working days. This year’s Spring Festival holiday lasted nine days, the longest in history, making it three days shorter than February 2025’s 19 working days. Due to subdued automotive consumption before and after the Spring Festival, most automakers take additional annual leave around this period. Therefore, February’s effective production and sales time will be very short, and the auto market’s sales volume is expected to hit the absolute low point of the year, potentially alleviating inventory pressure at the retail end.

The period before the Spring Festival has traditionally been a golden time for first-time car buyers, but in recent years, the proportion of first-time buyers has rapidly declined to less than 40%. Consequently, the pre-Spring Festival market momentum has continued to cool. Based on calculations from vehicle ownership and new registration data: In 2025, 13.19 million vehicles will be scrapped or transferred, with 13 million new purchases (17 million in 2024). Particularly, the entry-level fuel vehicle market remains weak, and consumer demand is lackluster ahead of the Spring Festival. Additionally, the overall cost of purchasing entry-level new energy vehicles has significantly increased compared to the previous year, dampening consumer willingness to buy cars for the holiday season.

The global surge in AI-driven demand for power storage has led to a sharp rise in the prices of non-ferrous metals, represented by copper, placing significant cost pressures on automakers. Following more than two consecutive years of explosive growth in new energy vehicle sales, the surge in prices of resources such as lithium carbonate has intensified upstream and downstream bargaining. It is expected that after the festival, the ability of new energy vehicle manufacturers to reduce prices for promotional purposes will decline. Weak price elasticity may lead consumers to adopt a cautious mindset, potentially suppressing normal vehicle purchase demand in the short term. The reversal of internal price competition is a long-term positive development, helping to alleviate观望情绪 (wait-and-see sentiment) and guide healthy industry consumption.

Amidst the positive progress of automotive tariff negotiations between China and Europe, as well as China and Canada, new energy vehicle exports have expanded from “pure vehicle sales” to “entire industrial chain exports.” Overall, it is projected that future automotive export growth will transition from rapid quantitative increases to qualitative leaps forward.