Key Stats for Tesla Stock

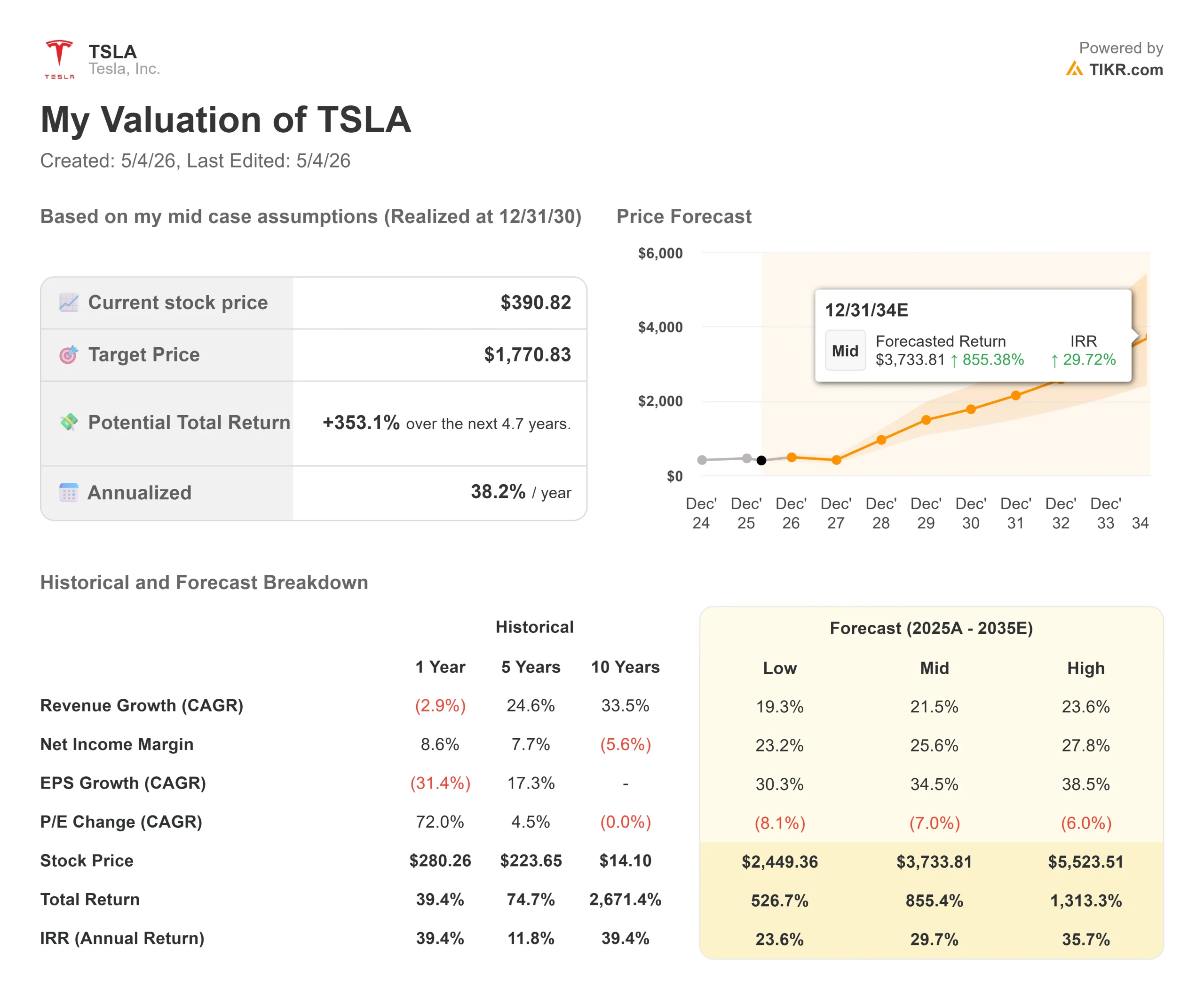

Current Price: $390.82

Target Price (Mid): ~$1,771

Street Consensus Target: ~$414

Potential Total Return: ~353%

Annualized IRR: ~38% / year

Earnings Reaction: -3.56% (April 22, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Tesla (TSLA) stock beat earnings estimates and got punished for it anyway. Shares fell 3.56% on April 23, closing at $373.60, despite Tesla’s strongest gross margin in five quarters and beats on both revenue and adjusted EPS. Bulls say Q1 confirms the AI platform pivot is intact. Bears say Tesla just told investors it will burn cash for the rest of 2026 while generating nothing material from Robotaxi or Optimus this year. The question the market is wrestling with: Does the spending Tesla is committing today produce the revenue growth the valuation demands by 2027?

What the Numbers Said and What the Market Heard

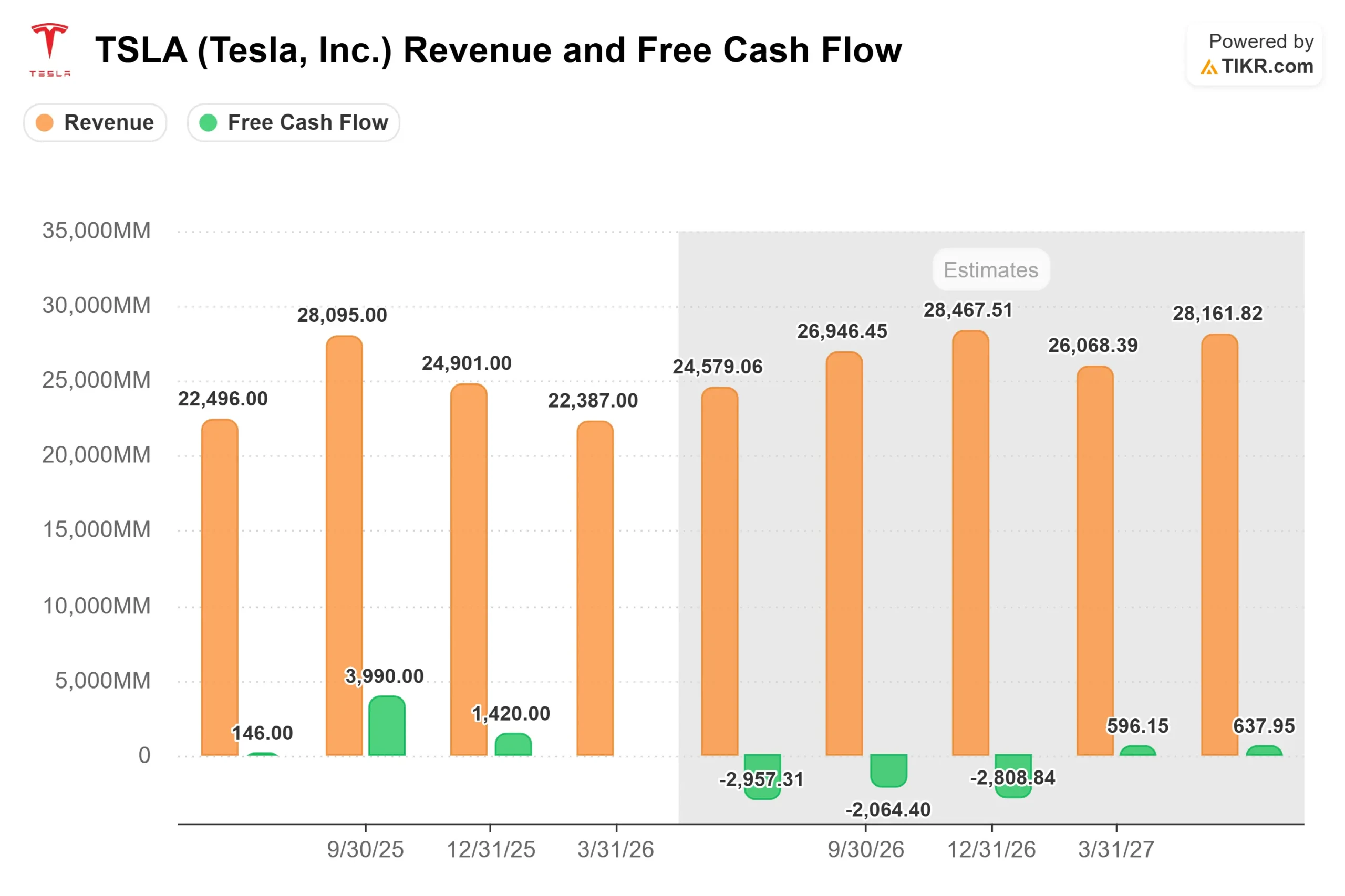

Tesla reported Q1 2026 actual revenue of $22,387 million against an average estimate of $22,208 million, per TIKR’s Beats & Misses data. Adjusted EPS came in at $0.41, beating the TIKR consensus estimate of $0.35 by 17.1%. Free cash flow for the quarter was just over $1.4 billion, per CFO Vaibhav Taneja on the earnings call.

Every income statement line was green. The stock still fell. The reason came from Taneja midway through the call: Tesla’s 2026 capital expenditure guidance was raised from $20 billion to over $25 billion, and free cash flow would be negative for the remaining three quarters of 2026. TIKR’s forward estimates confirm this: 2026 consensus FCF is projected at around negative $8.5 billion, with consensus CapEx around $23 billion. Tesla shares initially jumped roughly 4% after-hours on the earnings beat, then reversed once the capex number landed.

Taneja confirmed on the call that Tesla is simultaneously funding six factories moving toward operation, AI training compute, Cybercab and Semi production ramps, Optimus line installation in Fremont, and a semiconductor research fab in Austin. He added: “We’ll make such investments in a very capital-efficient manner.”

Tesla Revenue & Free Cash Flow (TIKR)

Tesla Revenue & Free Cash Flow (TIKR)

See historical and forward estimates for Tesla stock (It’s free!) >>>

What the Earnings Call Actually Revealed

CEO Elon Musk confirmed the last Model S and X vehicles will leave Fremont in early May. Disassembly of that production line is underway. The new Optimus line installation follows, with the start of production targeted for late July to August. Musk was direct about what comes next: “I don’t know what the production rate of Optimus will be this year. It is impossible to predict.” A second Optimus factory at Giga Texas targets production around summer 2027. His long-term view: Optimus is “probably the biggest product ever.”

Robotaxi service has expanded from Austin to Dallas and Houston, running on V14.3 software with zero incidents to date. Musk said the primary limiting factors are convenience issues, not safety vehicles occasionally getting stuck at complex intersections or looping in construction zones. He is targeting unsupervised FSD across roughly a dozen U.S. states by year-end, but was explicit that Robotaxi revenue will not be material in 2026. Meaningful contribution is expected in 2027.

The call’s most commercially sensitive disclosure. Musk confirmed that Hardware 3 vehicles sold with FSD packages between roughly 2019 and 2023 do not have the memory bandwidth required for unsupervised FSD. Tesla will offer discounted trade-ins and computer upgrades, but Musk said scaling retrofits would require building dedicated “micro factories” in major metro areas. The warranty reserve and customer liability implications have not yet appeared in the financials. Watch the Q2 10-Q.

CFO Taneja reported 1.28 million paid FSD customers globally, with Q1 growth driven by subscriptions and declining churn. FSD received regulatory approval in the Netherlands in Q1, with EU-wide approval expected in Q2 and broader China approval targeted for Q3.

Musk described a roughly $3 billion research semiconductor fab on the Giga Texas campus. Intel is partnering using its 14A manufacturing process. SpaceX will manage the initial phase of the larger-scale Terafab build. The motivation: Musk sees no path to sufficient AI chip supply at the volumes Tesla needs without making its own silicon.

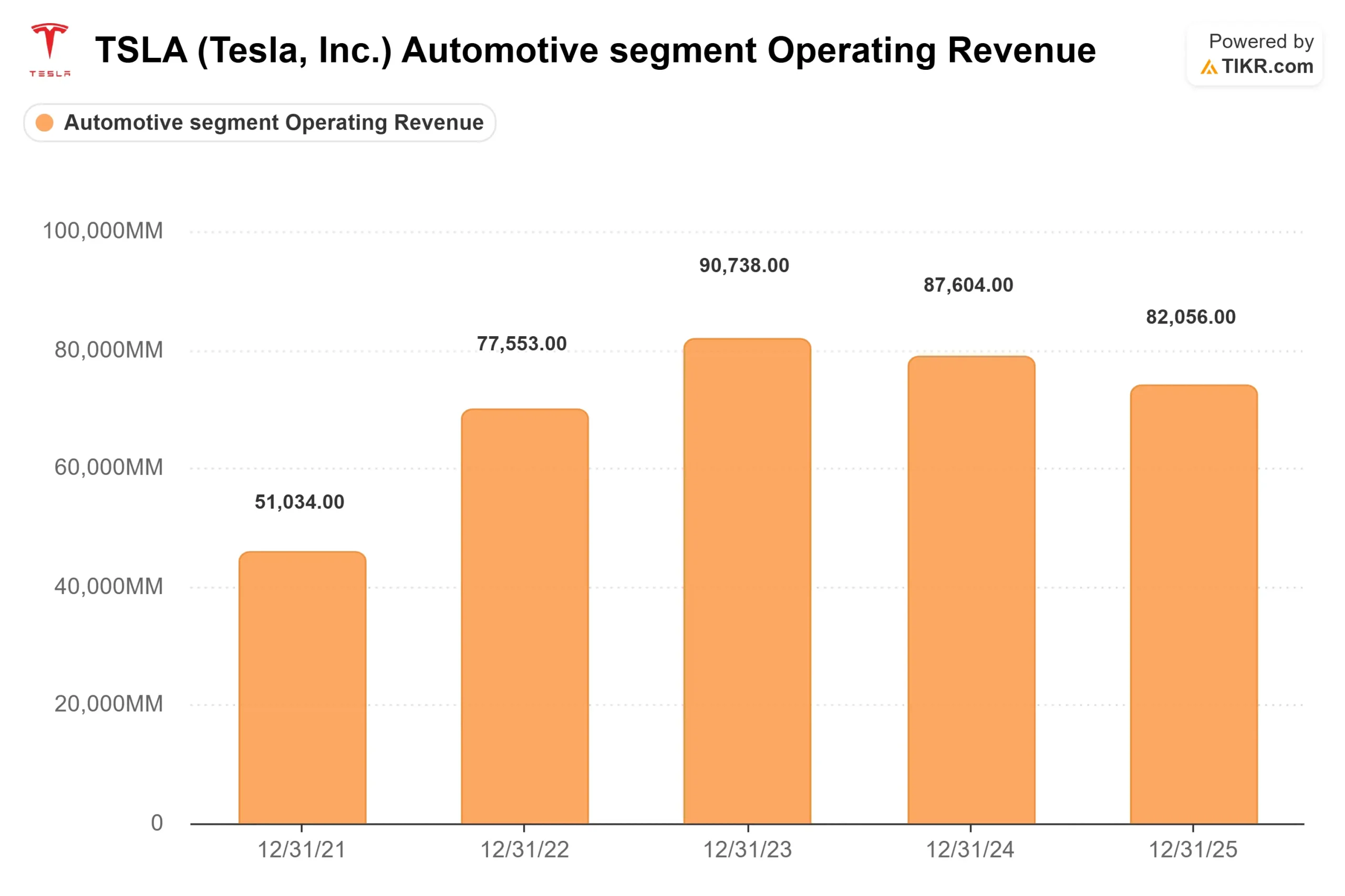

Tesla Automotive Operating Revenue (TIKR)

Tesla Automotive Operating Revenue (TIKR)

See how Tesla performs against its peers in TIKR (It’s free!) >>>

What the Valuation Is Actually Pricing

Per TIKR data as of May 1, 2026, TSLA trades at 87.2x NTM EV/EBITDA and 180.4x NTM P/E. Those are not automotive multiples. TIKR’s Competitors page shows BYD at 7.2x NTM EV/EBITDA and General Motors at 7.3x, with the peer median across comparable automobile companies at 7.2x. Tesla trades at more than 12 times that median.

The bear argument: Tesla’s LTM EBIT margin sits at 4.9% per TIKR, well below its 16.8% peak in 2022. The company is committing over $25 billion in capital this year to businesses that, by management’s own admission, won’t contribute materially until 2027.

The bull argument: no competitor is simultaneously building its own chips, humanoid robot factories, driverless taxi fleet, semiconductor fab, and FSD software stack. As Musk put it on the call: “I think it’s going to pay off in a very big way.”

That tension does not resolve this quarter. It resolves in 2027.

TIKR Advanced Model Analysis

Current Price: $390.82

Target Price (Mid): ~$1,771

Potential Total Return: ~353%

Annualized IRR: ~38% / year

Tesla Stock Price Target (TIKR)

Tesla Stock Price Target (TIKR)

See analysts’ growth forecasts and price targets for Tesla stock (It’s free!) >>>

The TIKR mid-case model prices Tesla at approximately $1,771 by December 31, 2030, around 353% total return and an annualized IRR of roughly 38% from the current price of $390.82. Two revenue CAGR drivers underpin the model: Robotaxi and FSD subscription scaling as autonomy approvals expand globally, and Optimus commercial revenue ramping from 2027 onward. The mid-case assumes around 22% revenue CAGR and net income margins expanding toward around 26% by 2030, per TIKR model data, as software-based revenue grows as a share of the mix.

The primary risk is timing. If Robotaxi monetization, Optimus deployment, and FSD global approvals each slip by 12 to 18 months, free cash flow deteriorates further, and multiple compression risk rises sharply. The TIKR low-case scenario projects approximately $2,449 by 12/31/30, still above today’s price over that 4.7-year horizon, but only if Tesla’s transition timeline broadly holds.

The Street’s consensus mean target of around $414 per TIKR implies modest upside from current levels, reflecting deep analyst disagreement: 18 Buys, 5 Outperforms, 17 Holds, 3 Underperforms, and 4 Sells, with targets ranging from $123 to $600. That five-to-one spread between low and high targets is itself the story: the market is not pricing a company right now. It is pricing a narrative.

Conclusion

Watch the auto gross margin excluding regulatory credits at Tesla’s Q2 2026 earnings on July 22. In Q1, it came in at 19.2%, aided by one-time warranty and tariff items, per CFO Taneja. A number above 18% without those tailwinds confirms core automotive profitability is genuinely improving. Below 18%, and the bear case gains traction: Tesla is spending over $25 billion this year on businesses that won’t contribute materially for at least another 12 months, while the car business funding all of it continues to weaken. Q2 needs to show the margin is real.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Tesla?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Tesla, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Tesla alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!