Although electric-vehicle (EV) stocks have cooled from their late-2023 highs, Tesla (TSLA) has been under particular pressure the most. After years of rapid growth, Tesla’s core auto business is bumping into stiff headwinds. Global EV sales are slowing, subsidies have faded, and competition is fiercer. For example, Tesla lost its EV sales crown last year to China’s BYD (BYDDY).

Investors are now questioning Tesla’s growth outlook even as the company pours resources into AI, robotics, and energy storage.

Amid this backdrop, after the Q delivery misses, JPMorgan reiterated a bearish stance, forecasting a 60% downside from current levels. Their renewed warning signals that Wall Street’s most bear-minded analysts still see trouble ahead for Tesla.

How Did Tesla Stock Perform?

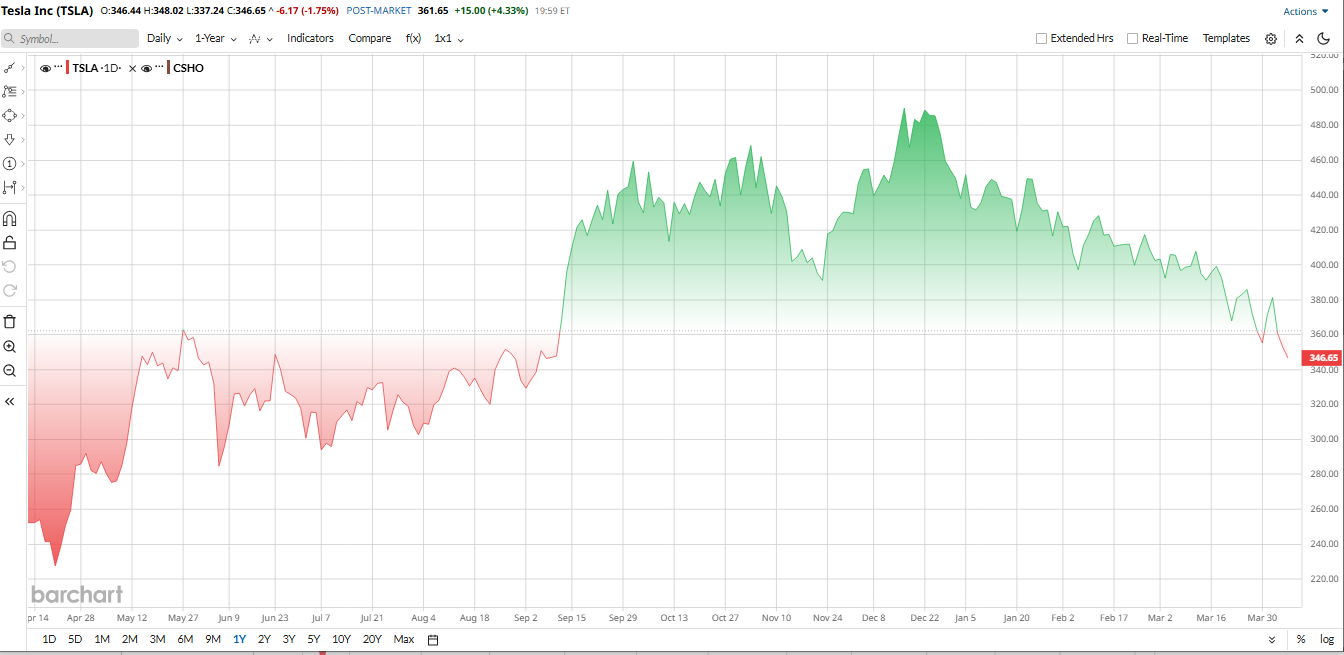

TSLA stock has been through a turbulent 12 months. After peaking near $500 in late 2025, shares slid into 2026 as delivery shortfalls and controversies weighed on confidence. Deliveries softened, culminating in Tesla’s first annual sales decline and a second consecutive year of lower volume.

As of early April 2026, TSLA is roughly 23% down year-to-date (YTD), giving back much of the 2025 rally. Technically, Tesla’s charts show strain. Barchart rates it mostly a “Sell” in the short term and notes the stock is bumping below its 50-day and 200-day moving averages. Traders see uncertainty that Tesla is no longer in a clear uptrend.

Moreover, despite the pullback, Tesla’s valuation looks very stretched. Its trailing P/E is sky-high, at 212x earnings, far above the sector median of 15x, as well as its own five-year historical average of 125x. However, as we know, Tesla trades like a high-growth tech stock, pricing in huge future wins. Bulls argue the premium is warranted by Tesla’s software edge and AI bets, but at face value, the stock is quite expensive relative to normal auto benchmarks.

www.barchart.com JPMorgan Doubles Down on “Sell” Call

www.barchart.com JPMorgan Doubles Down on “Sell” Call

The news that JPMorgan reiterated an “Underweight” (sell) rating on TSLA stock put it into a slump. The stock just hit its lowest 2026 level and shed over 7% in the past five days. Analyst Ryan Brinkman kept a $145 price target, which is about 60% below current levels. He warned that Tesla’s Q1 2026 deliveries were about 358,000, missing forecasts, and that earnings would drop.

Brinkman also cut his Tesla EPS forecasts sharply for Q1 to $0.30 from $0.43 and for FY 2026 to $1.80. JPMorgan says the stock is pricing in an unrealistic rebound, given a “record surge in unsold vehicles” and an inventory of 164,000 units.

For investors, JPMorgan’s note reinforces caution; it didn’t surprise anyone, but it reminds traders that one of the largest banks still sees Tesla as overvalued and likely headed lower.

Tesla’s Revenue Slips Amid Softer Vehicle Sales

Tesla’s recent financials underline the same story as JPMorgan cited. In full-year 2025, Tesla delivered about 1.63 million vehicles vs. 1.69 million in 2024. The fourth quarter of 2025 saw deliveries of 418,227, up 3% YoY.

Looking at the top line, revenue for Q4 2025 came in at roughly $24.5 billion, down a few percent year-over-year (YoY), reflecting slightly lower car sales.

On the profitability side, net income for Q4 was only about $0.8 billion, less than half of the prior year’s quarter. On a per-share basis, adjusted EPS was roughly $0.44, beating a consensus of $0.43 by a hair but still down sharply from the prior year.

At the same time, cash flow weakened. Tesla generated about $1.4 billion in free cash flow in Q4 versus $1.7 billion a year earlier, as working capital and investment needs absorbed cash. Cash and equivalents ended Q4 around $43.5 billion, still a massive war chest.

Despite these pressures, management maintained a cautiously optimistic tone. CEO Elon Musk and management offered a cautiously optimistic view for the future. In Tesla’s shareholder letter, Musk noted that “2025 marked a critical year” as the company pivots from being a hardware automaker to a “physical AI company.” The company touted progress on factories and new products, Cybercab (robotaxi) and Semi, expected in 2026.

Looking ahead, Analyst consensus sees Q1 2026 revenue around $24.0 billion and EPS roughly $0.24, well below year-ago levels. Tesla says it expects to keep growing deliveries slowly, but higher costs and competition will pressure margins in the near term.

Latest News and Developments

Aside from the quarterly numbers, several key developments are affecting Tesla in 2026. The first-quarter delivery miss of 358,000 vehicles highlighted a growing inventory buildup of over 50,000 unsold cars. U.S. EV incentives have expired, hurting demand, and regulatory issues like Europe’s delayed approval of Tesla’s “Full Self-Driving” software are also crimping sales.

On the flip side, there is something to cheer about as Tesla is pushing technology. It recently deployed the second generation of its in-house autonomous chip and has begun pilot production of a new 4680 battery cell at Giga Texas. In the energy segment, installations are normalizing after huge growth; Q1 deployments fell 15%.

Importantly, Tesla still has a very strong balance sheet to invest in. Musk’s side projects, SpaceX and xAI, continue drawing headlines. Investors are asking whether new products, Cybercab, Semi, and Optimus robots, can revive enthusiasm later this year.

Wall Street Take on TSLA Stock

Wall Street’s views on TSLA are now mixed-to-cautious. JPMorgan’s Ryan Brinkman remains the most bearish, sticking with an “Underweight” rating and $145 target. He warns of “elevated execution risk” and oversized expectations.

By contrast, some firms have trimmed but not cut ratings. Goldman Sachs cut its target to $375 with a “Hold” rating, noting weak EV sales and margin pressures. Truist lowered its target to $400 with a “Hold” rating for similar reasons. Baird’s Ben Kallo trimmed slightly to $538 with “Outperform,” essentially keeping his bullish call. Wedbush remains the outlier bull with a hold on its $600 target and a “Buy” after Q1 deliveries, citing “deliveries miss was not a surprise.”

Overall consensus as per Barchart is around a “Hold” with a 12-month median target near $405, implying roughly 17% upside potential over current levels.

www.barchart.com

www.barchart.com

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.