Tesla TSLA is out with its first-quarter 2026 delivery numbers and results were underwhelming, though not surprising. Deliveries in the quarter totaled 358,023 units (comprising 341,893 Model 3/Y and 16,130 Other Models), lagging the Zacks Consensus Estimate of 366,124. While deliveries rose modestly year over year, they declined sequentially from 418,227 units in the fourth quarter of 2025.

An aging lineup, lack of major new launches and intensifying competition — particularly from Chinese EV giant BYD Co Ltd BYDDY — are weighing on Tesla’s core electric vehicle (EV) business. The brand no longer commands the same dominance it once did. Notably, Tesla lost its global EV leadership to BYD last year, marking the first time it was overtaken on an annual basis. Deliveries have now declined for two consecutive years, with the pace of contraction accelerating—from a 1% drop in 2024 to more than 8% in 2025.

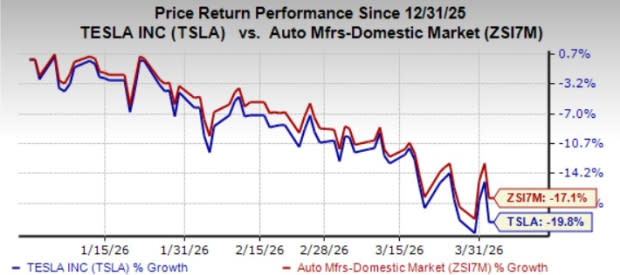

The slump has continued into 2026. Following the softer-than-expected delivery print, Tesla shares fell about 5% on Thursday, taking the year-to-date decline to nearly 20%.

Zacks Investment Research

Zacks Investment Research

Image Source: Zacks Investment Research

While Tesla’s core EV business faces mounting pressure, CEO Elon Musk is increasingly betting on autonomous vehicles (AVs) and artificial intelligence (AI) as the company’s next growth engines. However, meaningful monetization from these initiatives is still years away. This raises a key question for investors— should they exit TSLA amid near-term challenges, or stay invested for its long-term AI/AV-driven potential?

Tesla, Inc. Price, Consensus and EPS Surprise

Tesla, Inc. Price, Consensus and EPS Surprise

Tesla, Inc. price-consensus-eps-surprise-chart | Tesla, Inc. Quote

Tesla has ended production of its once-iconic Model S and Model X—vehicles that helped define its early brand identity but have now lost relevance amid a wave of more affordable EV options. These models, grouped under the “Other Models” category alongside Cybertruck, have increasingly become a drag on volumes.

Even the much-hyped Cybertruck has struggled to gain meaningful traction with consumers, raising questions about its long-term viability. Meanwhile, Tesla is now ramping up deliveries of its Semi truck, signaling a pivot toward commercial vehicles.

At the same time, Tesla is retooling its Fremont plant—previously home to Model S/X production—to support manufacturing of Optimus, its humanoid robot. The broader strategy is clear—move away from low-return luxury vehicles and redirect capital toward futuristic, high-growth opportunities like AI, robotics, and autonomy. However, execution risks remain high, and betting heavily on these still-evolving technologies may be premature at this stage.

Story Continues

Tesla’s ambitions in autonomous driving and robotics are bold, but the gap between vision and reality is still significant. The company launched its robotaxi service in Austin in June 2025 and has since expanded to the Bay Area, with plans to enter several more U.S. cities. CEO Elon Musk has suggested that, pending regulatory approvals, fully autonomous vehicles could reach up to half of the U.S. population by year-end. However, given previously missed timelines, such projections warrant caution.

Competition is intensifying as well. Alphabet’s GOOGL Waymo currently leads the U.S. robotaxi market, operating in multiple cities with Level 4 autonomous technology—capable of functioning without human intervention in designated zones. Tesla, by contrast, remains at Level 2 automation, which still requires active driver supervision. The scale gap is also notable. Tesla has logged nearly 700,000 paid miles to date (as highlighted on its last earnings call), while Waymo is already handling more than 450,000 paid rides per week.

Adding to the uncertainty is Tesla’s aggressive spending plan. The company expects capital expenditures to exceed $20 billion in 2026—more than double last year’s levels. These investments will fund multiple new facilities and AI infrastructure, even as the core EV business shows signs of slowing, increasing the overall risk-reward imbalance in the near term.

Based on its price/sales ratio, the company is trading at a forward sales multiple of 12.78, way higher than the broader industry and its own 5-year average. Tesla’s valuation has historically remained disconnected from near-term fundamentals, but that does not eliminate downside risk. Much of the optimism surrounding its long-term autonomy and AI bets is already priced in. TSLA carries a Value Score of F.

Zacks Investment Research

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for TSLA’s 2026 and 2027 EPS have moved south over the past seven days by one cent each.

The risk-reward for Tesla stock now looks unfavorable. Its core business is slowing and the company is pouring heavy capital into areas that may take years to deliver results. While new frontiers like robotics and autonomy could open up a massive long-term opportunity, questions around cost efficiency and scalability are yet to be answered, making it far from a near-term revenue driver.

At the same time, the stock still trades at a rich valuation, leaving little margin for error. Unless Tesla shows clear improvement in its core operations or meaningful progress in new businesses, the downside risk remains high. In our view, Tesla is best avoided at the moment.

The stock carries a Zacks Rank #5 (Strong Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Tesla, Inc. (TSLA) : Free Stock Analysis Report

Alphabet Inc. (GOOGL) : Free Stock Analysis Report

Byd Co., Ltd. (BYDDY) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).