Support CleanTechnica’s work through a Substack subscription or on Stripe.

Plugin vehicle registrations were down 11% year over year (YoY) in February, ending the month close to 1.1 million units. Both BEVs (-8% YoY) and PHEVs (-16% YoY) had sales drops. This is the worst drop since the COVID-19 era, but there is one easy explanation for this — incentives. Or the end of them.

The end of US incentives last October, added to the partial removal of incentives in China at the end of 2025, had an expected impact, as these are the 3rd and 1st largest EV markets, respectively.

Actually, if we remove China and the USA from the tally, EVs have jumped 36% YoY globally, with BEVs growing slightly faster (+39%) than PHEVs (+30%).

Just because certain media-friendly markets are down, that doesn’t mean that all markets are down.

So, Keep Calm and Carry On, the EV Revolution is in good health, and with what is happening in the Middle East, ICE sales are going to melt faster, to the profit of plugins.

Share-wise, February saw BEVs end the month at 11% share, with the tally increasing to 16% if we add in PHEVs. This performance pushed the 2026 plugin share slightly downward, because while BEVs kept their share at 12%, plugin hybrids lost one percentage point, going from 6% in January to their current 5% share. Therefore, the 2026 PEV share was at 17%.

For reference, 2025 market share ended with BEVs at 17% share and all plugin vehicles combined at 26%. Although we are still far from those results, comparing where we are now to where we were twelve months ago, the difference is much smaller (13% BEV share then vs. 12% now), so I am expecting that the second half of the year will bring robust growth again, with BEVs probably north of the 20% share barrier by the end of the year.

With the domestic market of Chinese OEMs suffering from the loss of incentives, and linked to the long holidays of the Spring Festival, the Chinese EV market became less dominant globally, dropping to 43% of global sales, its lowest share in years. And that shows in the top 20….

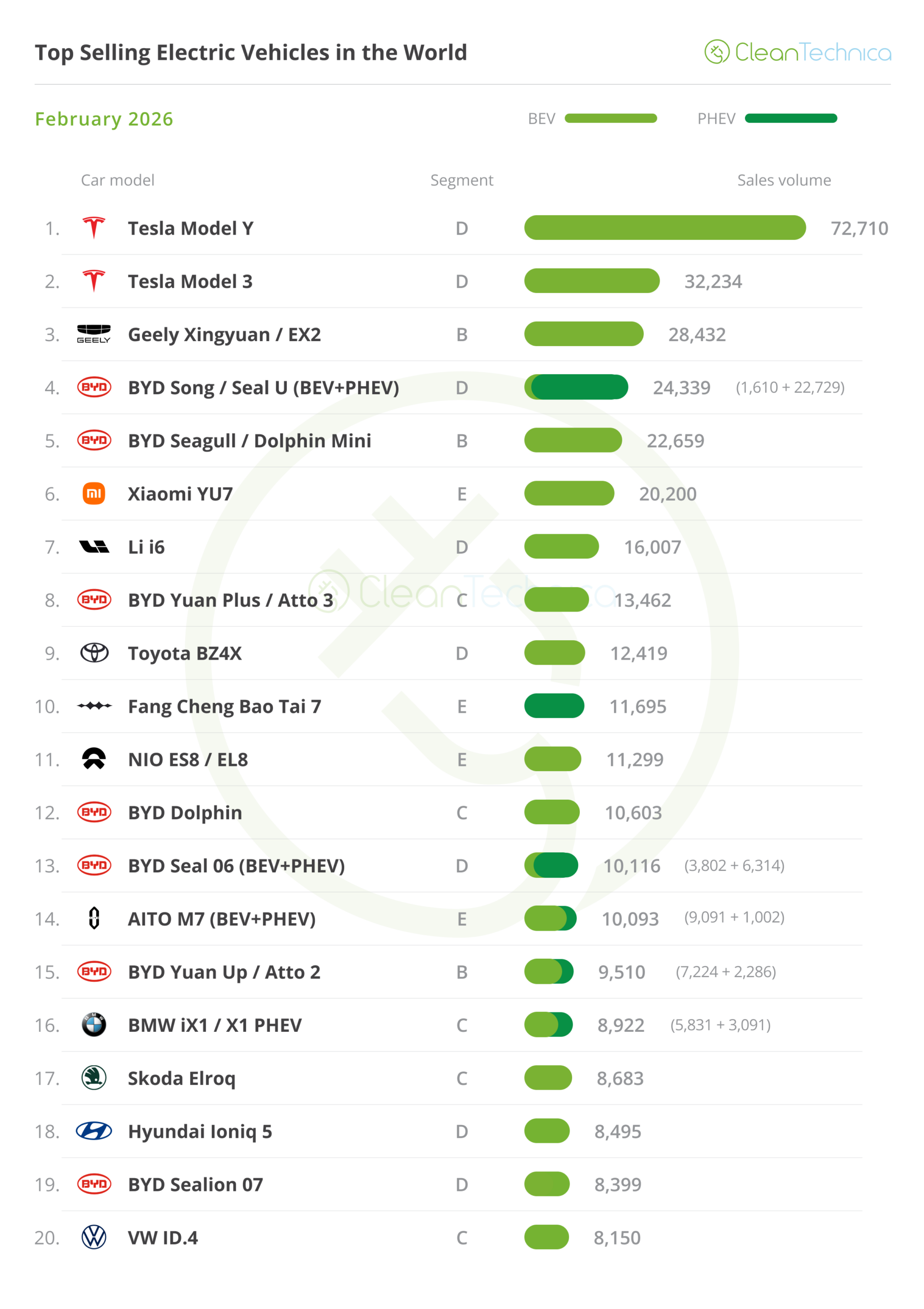

Looking at the best selling models, with slow Chinese sales, it was a great opportunity for foreigners to shine, as one can see at the top with Tesla taking the #1 and #2 spots in a non-peak month, for the first time in years!

Still, the leader Model Y and runner-up Model 3 had contrasting performances YoY. While the crossover grew 53% YoY to 72,710 units, no doubt helped by the fact that a year ago its production was hampered by the refresh change, the sedan saw its sales drop by 23% YoY — to 32,234 units. Ouch.

Still, this was enough to keep the competition behind it, like the Geely Xingyuan (EX2 in export markets), which completed the podium with close to 29,000 registrations. Geely’s small EV is now at cruising speed, compensating for the loss of demand in its domestic market with increased exports.

But the highlight in the first half of the table goes to … the Toyota BZ4X!

Yep, for the first time in many, many years, we have a Toyota in the top 10, thanks to a record 12,419 registrations. It got up to the 9th spot on the table. Thanks to the recent refresh, which, among other things, lowered the price and finally gave it decent specs, the Japanese SUV was the best selling legacy model. Sales were distributed across a number of markets, with four of them reaching above 1,000 sales (Japan, Denmark, Canada, and the USA).

Are these the first signs that Toyota is finally awakening?

In the second half of the table, the sales drop in China allowed more legacy models to show up on the table, making it a total of five this month. Highlights included the #16 BMW X1 PHEV/iX1 twins, the #17 Skoda Elroq, and the #18 Hyundai IONIQ 5, with the Korean growing 30% YoY. Overall, it was a positive month for Hyundai–Kia, as it saw a few more models shine, especially on the Kia side: the EV5 (4,512 units) crossover broke its personal record, while the EV4 (3,209 units) continued to ramp up production, with the same story happening to the passenger version of the PV5 (3,372) MPV.

Funny enough, the usual leader among legacy EVs, the VW ID.4, was only #20 in February. The crossover was no doubt suffering from the Osborne effect due to the upcoming ID.Cross and its own successor, the future ID.Tiguan.

Outside the top 20, the highlights come from Asia. Leapmotor’s small T03 ended fewer than 200 units behind a top 20 position, thanks to 7,978 sales, its best result in over two years — with the majority of sales coming from just one market (Italy). Meanwhile, the Kia EV3 (7,135 units) and Chery’s Jaecoo 5 EV (7,065) also shined, with this last one owing his success to just two countries — more than 80% of its sales were concentrated in Indonesia and Thailand.

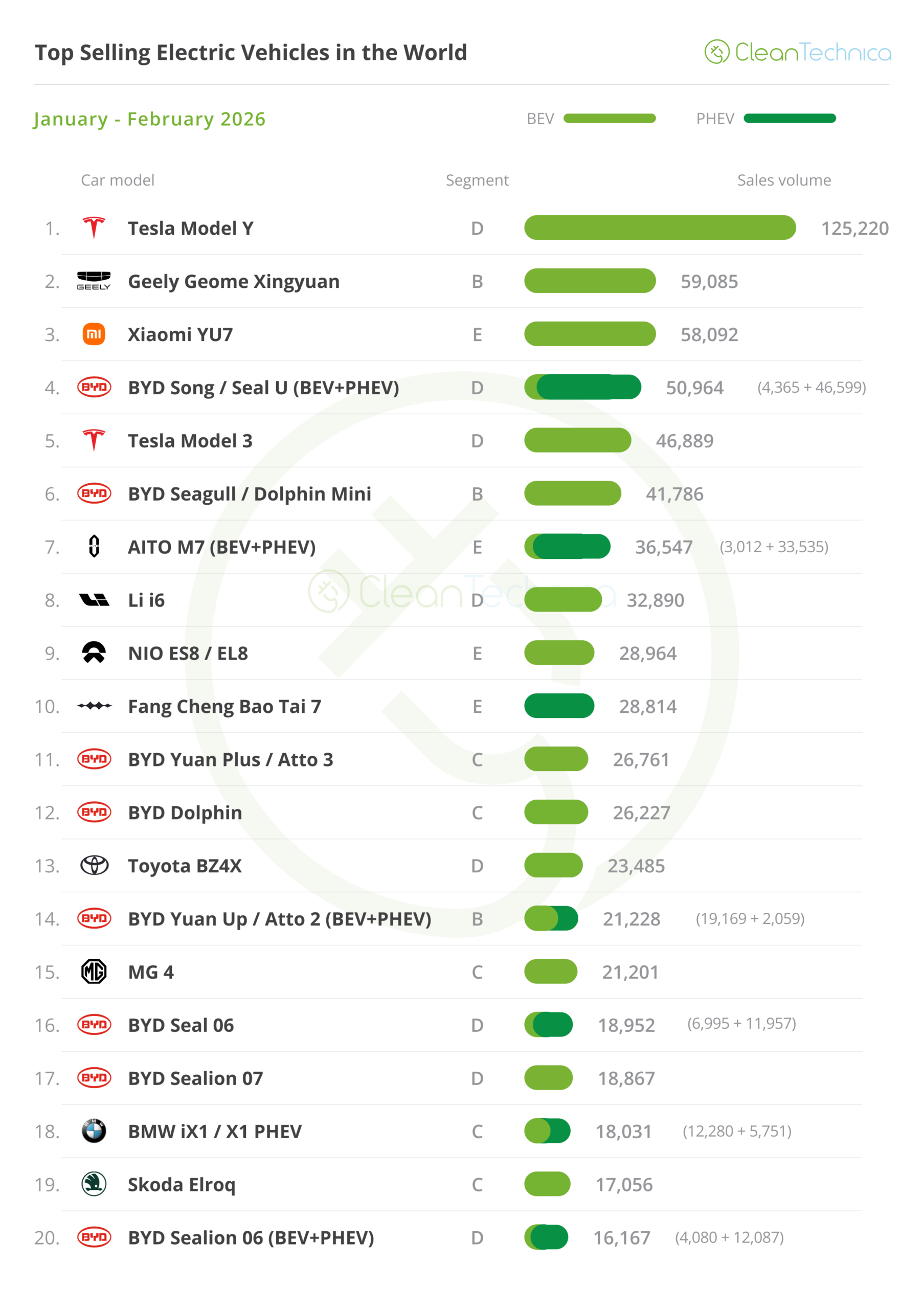

Year to date, the small Geely Xinguan has surpassed the Xiaomi YU7 and is the new runner-up. Below the podium, last year’s big sellers are recovering their spots after a slow January. The BYD Song was up one position, to 4th, while the Tesla Model 3 jumped five positions, into the 5th position.

With sales down 30% so far this year, one wonders how high Tesla’s sedan will climb in March thanks to Tesla’s expected sales peak. Surpassing the BYD Song? That should be easy, as the veteran model is fading out. Xiaomi’s YU7? Hmm…. Maybe, maybe not. I would say there is a 50/50 chance. As for the small Geely hatchback, I seriously doubt it. Not only does the Chinese EV have a comfortable advantage of 13,000 units, but the Model 3 no longer has the extreme high tides of the past, so realistically, racing to keep the 3rd position is the best that the Tesla midsizer can expect. And even that is far from being assured….

Further below, Li Auto’s i6 midsizer climbed another position, to 8th, confirming its popularity, while in the second half of the table, BYD is slowly pushing upwards, with four models (Yuan Plus, Dolphin, Seal 06, Sealion 06) climbing positions.

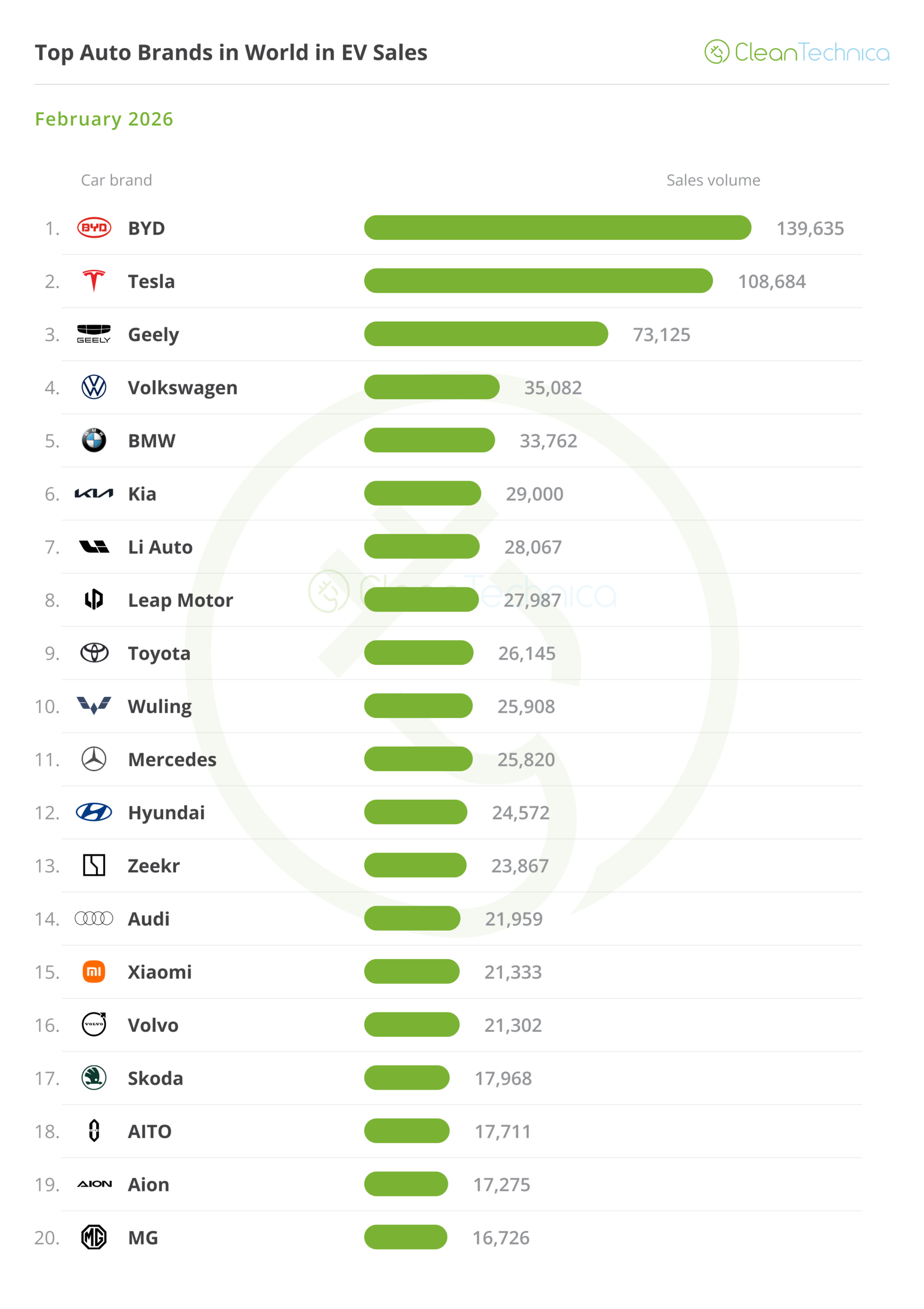

Manufacturers: Kia shines in a normal month

Nothing really out of the ordinary happened in the top positions, with BYD, Tesla and Geely taking over the podium, followed by #4 Volkswagen and #5 BMW fighting it out for the best legacy make title.

Having said that, Wuling’s absence is noteworthy. It ended the month in only 10th, no doubt still reeling from the subsidies cut to its cheaper models. On the other hand, the Climber of the Month was the Korean Kia, which ended the month in 6th, its highest standing in years. With a number of the EVx and PVx models still ramping up and/or being introduced, one can be optimistic about Kia’s prospects for this year.

Regarding the remaining positions on the table, another surprise was Toyota’s #9 position. Will 2026 be the year that the giant awakens?

I mean, it feels strange to celebrate a top 10 presence in the EV arena when you are the best selling automotive brand in the world….

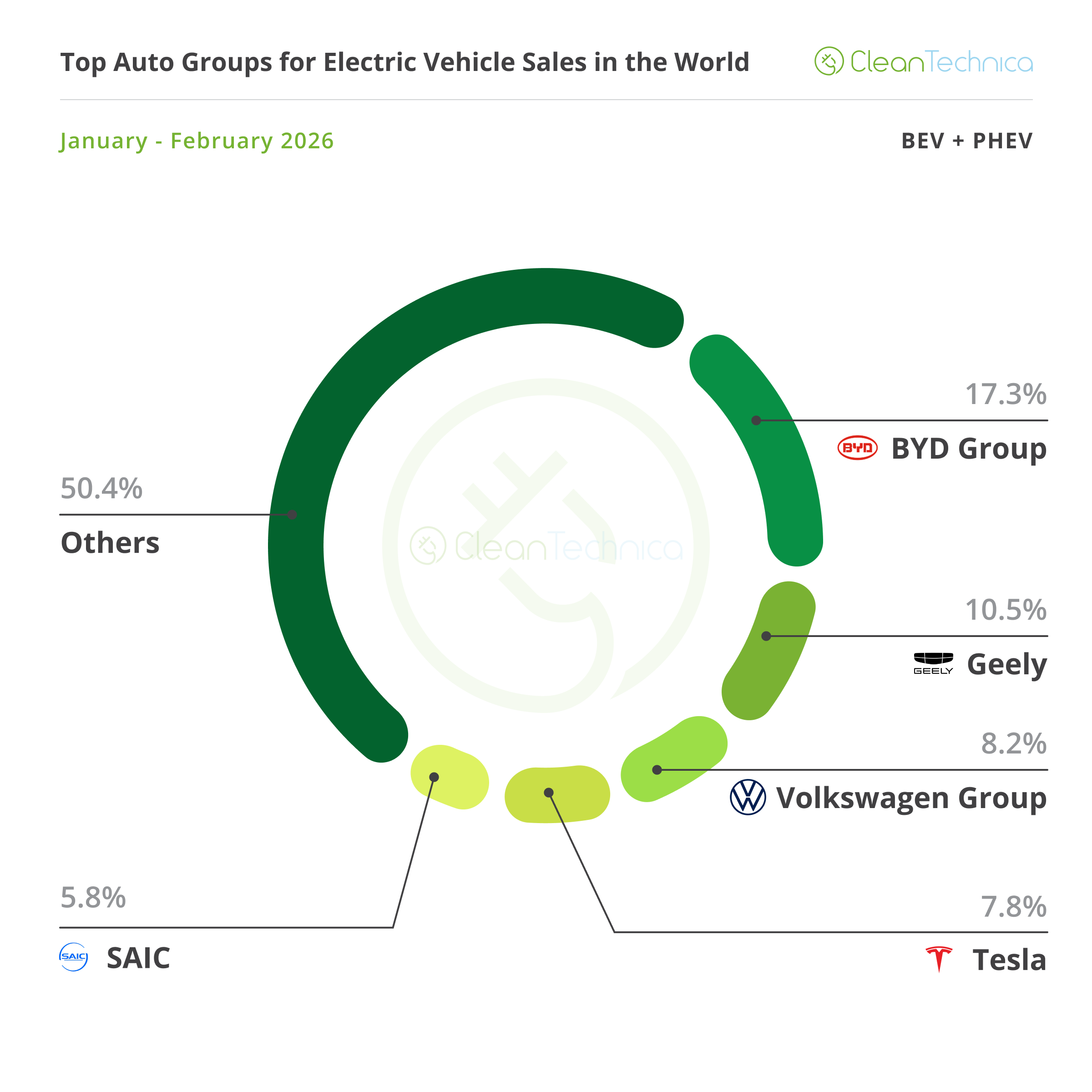

As for the year-to-date table, Tesla has surpassed Geely and returned to the runner-up position, with #4 Volkswagen and #5 BMW also celebrating their return to the top 5, after being briefly surpassed by Xiaomi. Still, the Chinese OEM spent February on the process of refreshing its sedan model, the SU7. With this in mind, expect Xiaomi to go back on the offensive in the coming months, and I wouldn’t be surprised to see it competing with the Germans for the 4th position in the near future.

With Kia taking the 6th position in February, the Korean make jumped five positions up the top 20, ending the second stage of the race at #13. Is Kia on its way to a top 10 position?

Looking at OEMs, BYD (17.3%, down from 17.4% in January 2026) is stable in the lead, while runner-up Geely (10.5%) is also stable.

Tesla (7.8%, up from 6% in January) is now recovering lost ground, having surpassed SAIC (5.8%, down 0.4%) to become the 4th placed OEM on the table.

But Tesla’s true goal is to recover the bronze medal from #3 Volkswagen Group (8.2% now vs 8.1% in the previous month).

Expect the usual Tesla high tide in March, which will likely help it surpass the 9,000 units that separate it from the German OEM and join the podium at the end of the quarter. The thing is … it is not a given. It will depend on the size of that high tide.

This is Tesla’s new reality, competing for the 3rd position with a legacy OEM. (Eww…)

But I digress. Outside the top 5, Hyundai–Kia (4.2%, up from 3.6% in January) took profit from the weak moment of the Chinese market to increase its lead over #7 Chery (3.8%) and #8 BMW Group (3.6%).

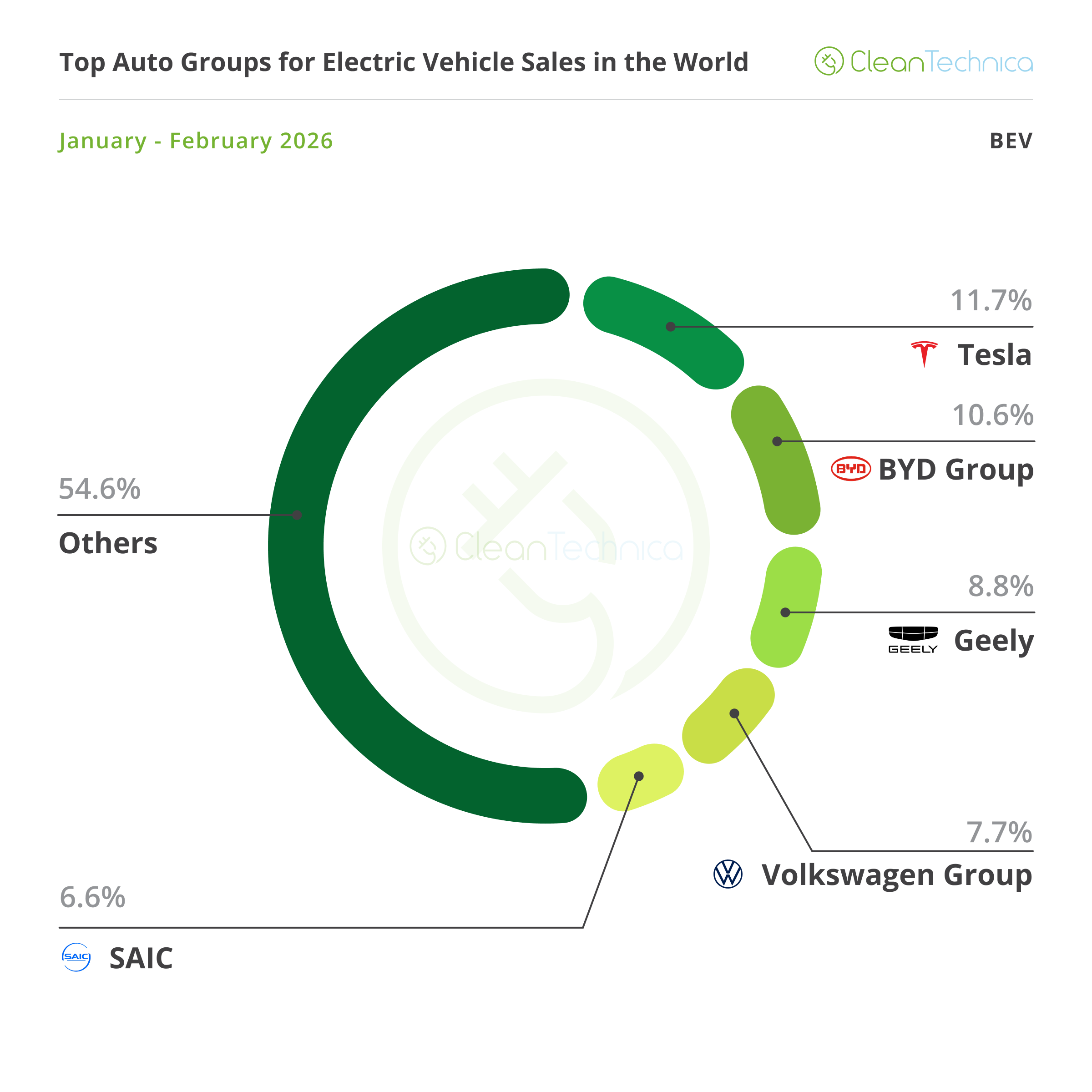

Looking just at BEVs, there were 1.5 million registrations in the first two months of 2026, or 67% of total plugin sales.

We have a surprise at the top, with Tesla (11.7%) taking the lead!

Sure, this shouldn’t last long. I would say until April. But, still, a win is a win, right?

With buyers waiting for BYD (10.6% share) to launch the second generation of its Blade Battery, its BEV sales have fallen, but expect sales to pick up again, as it seems BYD is all in on its new battery tech and that should allow it to regain the leadership position soon.

In 3rd place we have a stable Geely (8.8%), followed by #4 Volkswagen Group (7.7%, down 0.2% share) and #5 SAIC (6.6%, down 0.7% compared to January), which is still suffering from Wuling’s bad results.

Outside the top 5, a rising Hyundai–Kia (5.2% share, up from 4.3% in January) has surpassed Xiaomi and is the new 6th placed OEM — but it is still far from a top 5 position.

The Korean OEM should instead keep an eye on Xiaomi, as the startup will surely win market share in the coming months and could surpass Hyundai–Kia soon.

Sign up for CleanTechnica’s Weekly Substack for Zach and Scott’s in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News!

Advertisement

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica’s Comment Policy