Find winning stocks in any market cycle. Join 7 million investors using Simply Wall St’s investing ideas for FREE.

Tesla, Inc. (NasdaqGS:TSLA) reported Q1 2026 vehicle deliveries that missed its own targets, contributing to an inventory buildup of over 50,000 vehicles produced but not yet sold.

The company also reported a 38% sequential decline in energy storage deployments in the quarter, after this segment had been framed as a key part of its diversification beyond autos.

These developments arrive as Tesla highlights AI, robotics, and physical autonomy as future areas of focus, which raises questions about demand strength in its established businesses.

Tesla remains primarily an electric vehicle and energy storage company, even as interest in its AI and robotics ambitions grows. For investors, Q1 2026 puts the core car and energy operations back at the center of the conversation, with attention on how inventory, pricing decisions, and product mix may influence the next few quarters. The energy storage slowdown adds another layer, since this business had been positioned as a key complement to vehicle sales.

Looking ahead, the key questions are how quickly Tesla can rebalance production and deliveries, and whether energy deployments stabilize or continue to fluctuate. Investors will likely watch for management commentary on priorities between autos, energy, and newer AI or robotics efforts, along with any updates on capital allocation between these areas.

Stay updated on the most important news stories for Tesla by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on Tesla.

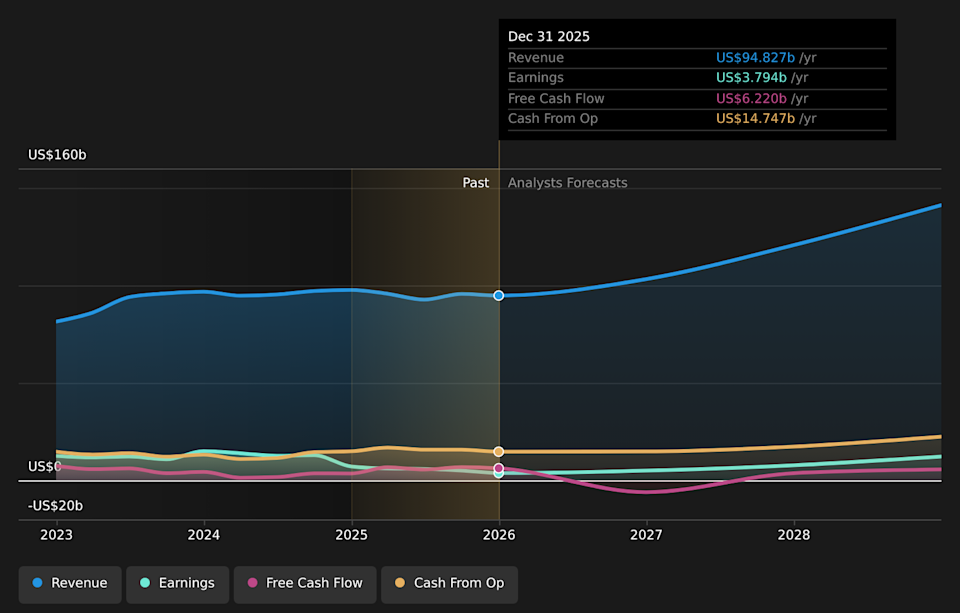

NasdaqGS:TSLA Earnings & Revenue Growth as at Apr 2026

NasdaqGS:TSLA Earnings & Revenue Growth as at Apr 2026

The Q1 2026 update puts the focus squarely back on Tesla’s ability to generate cash from its core operations, which matters for any future income stream such as dividends. Producing over 408,000 vehicles but delivering just over 358,000, and reporting 8.8 GWh of energy storage deployments, points to softer demand than Tesla and the market had expected, with inventory rising and a key growth segment cooling off. For current and prospective shareholders, that combination can weigh on margins and free cash flow, especially while Tesla is committing large amounts of capital to AI chips, robotaxis, and humanoid robots. The company does not currently pay a dividend, so this news is less about a direct income setback and more about what it may signal for the timing and sustainability of any future payout policy. If the auto and energy businesses require more price cuts or heavier investment to clear stock and reaccelerate growth, management may have fewer options to return cash to shareholders, and may instead prioritize funding high capex projects over introducing or increasing dividends.

The softer Q1 deliveries and energy deployments test the idea in the narrative that expanding energy storage and AI powered services will steadily support higher margins and a stronger cash base over time.

Rising vehicle inventory and a sequential drop in energy storage volumes challenge confidence that existing auto and storage operations can comfortably fund large AI, robotics, and factory build outs without putting pressure on profitability.

The narrative focuses heavily on long term autonomy and energy catalysts and does not fully reflect how a period of weaker volumes and possible margin strain could affect the company’s flexibility to introduce dividends or other cash returns in the medium term.

Knowing what a company is worth starts with understanding its story. Check out one of the top narratives in the Simply Wall St Community for Tesla to help decide what it’s worth to you.

⚠️ A second consecutive delivery miss, combined with more than 50,000 vehicles produced but not yet sold, can pressure pricing and margins, which may limit room for shareholder returns and extend the timeline for any dividend policy.

⚠️ A 38% sequential decline in energy storage deployments removes a potential offset to a softer auto segment and adds uncertainty around how consistently this business can contribute to cash generation.

🎁 Tesla still delivered 358,023 vehicles, and 6.3% year on year growth shows the auto franchise retains scale that could support future dividends if profitability and cash flow stabilize.

🎁 Management’s continued commitment to AI, robotics, and dedicated chip capacity, if executed well relative to peers such as BYD, Rivian, and legacy automakers, could eventually create higher margin revenue streams that improve the company’s ability to consider income distributions.

From here, pay close attention to Tesla’s Q1 2026 earnings release and cash flow statement, not just the delivery and deployment numbers that have already been disclosed. Investors should look for management commentary on pricing, inventory clearing plans, and how capital is being allocated between autos, energy storage, and AI or robotics projects. Any guidance on margin trends and capex for 2026 will be important for judging how much financial flexibility Tesla has to support both growth projects and potential future income returns. It is also worth tracking how competitors such as BYD and traditional automakers adjust pricing and product launches in key regions, because that competitive context will influence Tesla’s ability to protect profitability.

To ensure you’re always in the loop on how the latest news impacts the investment narrative for Tesla, head to the community page for Tesla to never miss an update on the top community narratives.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include TSLA.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Investors Should Pay Attention")