Support CleanTechnica’s work through a Substack subscription or on Stripe.

Big Players down, Hot Startups up

Plugin vehicle registrations were down 6% year over year (YoY) in January, ending the month close to 1.2 million units. Both BEVs (-4% YoY) and PHEVs (-8%) had sales drops. This is a rare occasion where plugin sales are down in both powertrains, but there is one easy explanation for this — incentives. Or the end of them.

The end of US incentives last October, added to the partial removal of incentives in China at the end of 2025, made an expected impact, as these are the 3rd and 1st largest EV markets, respectively.

Actually, if we remove China and the USA from the tally, EVs have jumped 36% YoY globally, with BEVs growing slightly faster (+37%) than PHEVs (+34%).

So, Keep Calm and Carry On, the EV Revolution is in good health, despite what some naysayers might proclaim….

Share-wise, 2026 started with plugin vehicles getting 18% share of the global auto market (12% BEV). The global market was helped by significant volumes in markets outside the spotlight, which are on the upswing. Just looking at markets registering more than 1,000 units in January, there is a constellation of countries with 100%-plus growth rates, a majority of them in Asia. That includes India, Indonesia, Malaysia, the Philippines, Singapore, and South Korea, but elsewhere there were also the cases of Azerbaijan, Belarus, Poland, and Uruguay.

Just because certain media-friendly markets are down, it doesn’t mean that all markets are down….

With Chinese OEMs now focusing on exporting their EVs as they try to win abroad the profits they are missing at home (due to the razor thin margins there), this is leading to a number of consequences in these export markets.

First, prices are dropping. More choice and cheaper models are helping EVs to expand their market share, at the cost of legacy OEMs’ ICE models.

At the same time, most legacy OEMs either see their EV models being obliterated in these markets (over 90% of the Brazilian EV market belongs to Chinese OEMs), or they are forced to play ball and drop prices in order to have a fighting chance to fend off the Chinese competition.

Last month, BEVs had over 774,000 registrations, placing the BEV share within plugins at 65%, in line with what was happening a year ago.

With the Chinese EV market in hangover mode over the cut to incentives, this market’s importance became less dominant globally, dropping from 59% of all global sales of electric cars in January 2025 to 51%.

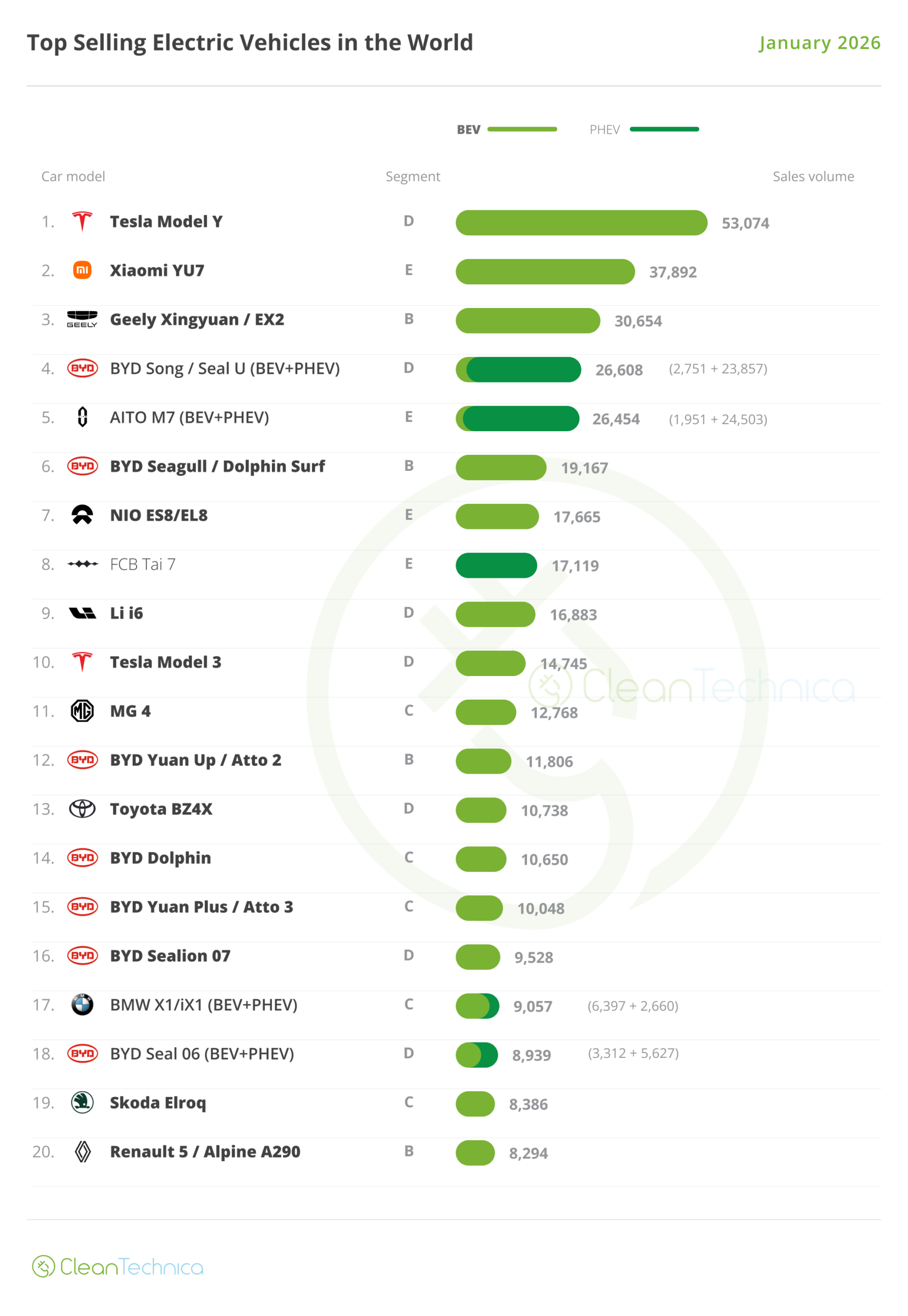

Looking at the best selling models, the Model Y started the race in its usual #1 spot, but it has seen its sales drop by 7% year over year, to 53,074 units.

Still, this was enough to have a comfortable 15,000-unit advantage over the runner-up model, where we have a surprise — the Xiaomi YU7 won silver! The Geely Xingyuan (EX2 in export markets) completed the podium, with close to 31,000 registrations, a 9% progression over January ’25.

So … will any of these Chinese EVs be able to challenge the supremacy of the Tesla Model Y? Hmm … not yet. The Xiaomi crossover is basically only sold in China, so its sales potential is currently cut in half, while the Geely hatchback is only now starting to get exported, so while there is potential to compete head to head with the Texan, I believe the conditions for such an event will only come about next year, in 2027.

So the Tesla Model Y is set to win its 5th consecutive Best Seller trophy this year.

The same cannot be said about its older sibling, the Model 3. Tesla’s sedan deliveries crashed in January, falling 47% YoY to fewer than 15,000 units, its worst result since April 2020, at the height of the COVID days….

This means that the sedan started the year in 10th, its lowest standing since January 2018, when it was still in production hell and starting to spread its wings….

And let’s not forget that the sedan is now on its 9th year.

Away from the podium, the highlight is the massive AITO M7, which started the year in 4th, just ahead of the 2025 silver medalist, the #5 BYD Song. The veteran model was another model crashing in January, with the SUV falling 44% YoY to 26,608 units. While the Song is slowly disappearing from its domestic market, the midsizer is still quite popular in overseas markets, with these markets now representing 66% of the Song’s January total sales.

In more proof that the market was disrupted by the incentives cut, we have four full size Chinese EVs in the top 10. Besides the aforementioned Xiaomi YU7 and AITO M7, we also have the NIO ES8, in 7th, and the Fang Cheng Bao Tai 7, in 8th.

Oh, and in 9th we have another surprise. Li Auto’s i6, its fully electric MPV-SUV midsizer, scored 16,883 registrations, highlighting a trend that was starting to show towards then end of last year — the Chinese startups are disrupting the market, not only regarding foreign OEMs, but also regarding the big Chinese players.

This January, we have five startup models in the top half of the table, versus just one (Xiaomi SU7) a year ago.

Rank

Model

Seg

January

%

1

Tesla Model Y

D

53,074

4.5%

2

Xiaomi YU7

E

37,892

3.2%

3

Geely Xingyuan / EX2

B

30,654

2.6%

4

AITO M7 (BEV+PHEV)

E

26,454

2.2%

5

BYD Song / Seal U (BEV+PHEV)

D

26,608

2.2%

6

BYD Seagull / Dolphin Surf

B

19,167

1.6%

7

NIO ES8/EL8

E

17,665

1.5%

8

FCB Tai 7

E

17,119

1.4%

9

Li i6

D

16,883

1.4%

10

Tesla Model 3

D

14,745

1.2%

11

MG 4

C

12,768

1.1%

12

BYD Yuan Up / Atto 2

B

11,806

1.0%

13

Toyota BZ4X

D

10,738

0.9%

14

BYD Dolphin

C

10,650

0.9%

15

BYD Yuan Plus / Atto 3

C

10,048

0.8%

16

BYD Sealion 07

D

9,528

0.8%

17

BMW X1/iX1 (BEV+PHEV)

C

9,057

0.8%

18

BYD Seal 06 (BEV+PHEV)

D

8,939

0.8%

19

Skoda Elroq

C

8,386

0.7%

20

Renault 5 / Alpine A290

B

8,294

0.7%

Others

822,461

69.5%

TOTAL

1,182,936

100%

In the second half of the table, the sales drop in China allowed some European models to show up in the top 20, with the last three spots of the table going to the #18 BMW X1 PHEV/iX1 twins, the #19 Skoda Elroq, and the #20 Renault 5/Alpine A290 twins.

But funny enough, the leader among legacy OEMs hasn’t landed in Europe, but in Japan — the refreshed BZ4X (great password, BTW), jumped into 13th, thanks to 10,738 registrations, the SUV’s best result in 9 months.

Outside the top 20, the highlights come from China, with two models showing top 20 potential. One is Wuling’s Starlight 730, a midsize MPV that is ramping up production, having reached close to 8,000 units. It is already being exported to Indonesia and Thailand. The other is the Zeekr 7X, a very competent midsize SUV that should start to profit from export volumes this year. It reached 8,104 deliveries in January.

Manufacturers: Big Players down, Hot Startups up

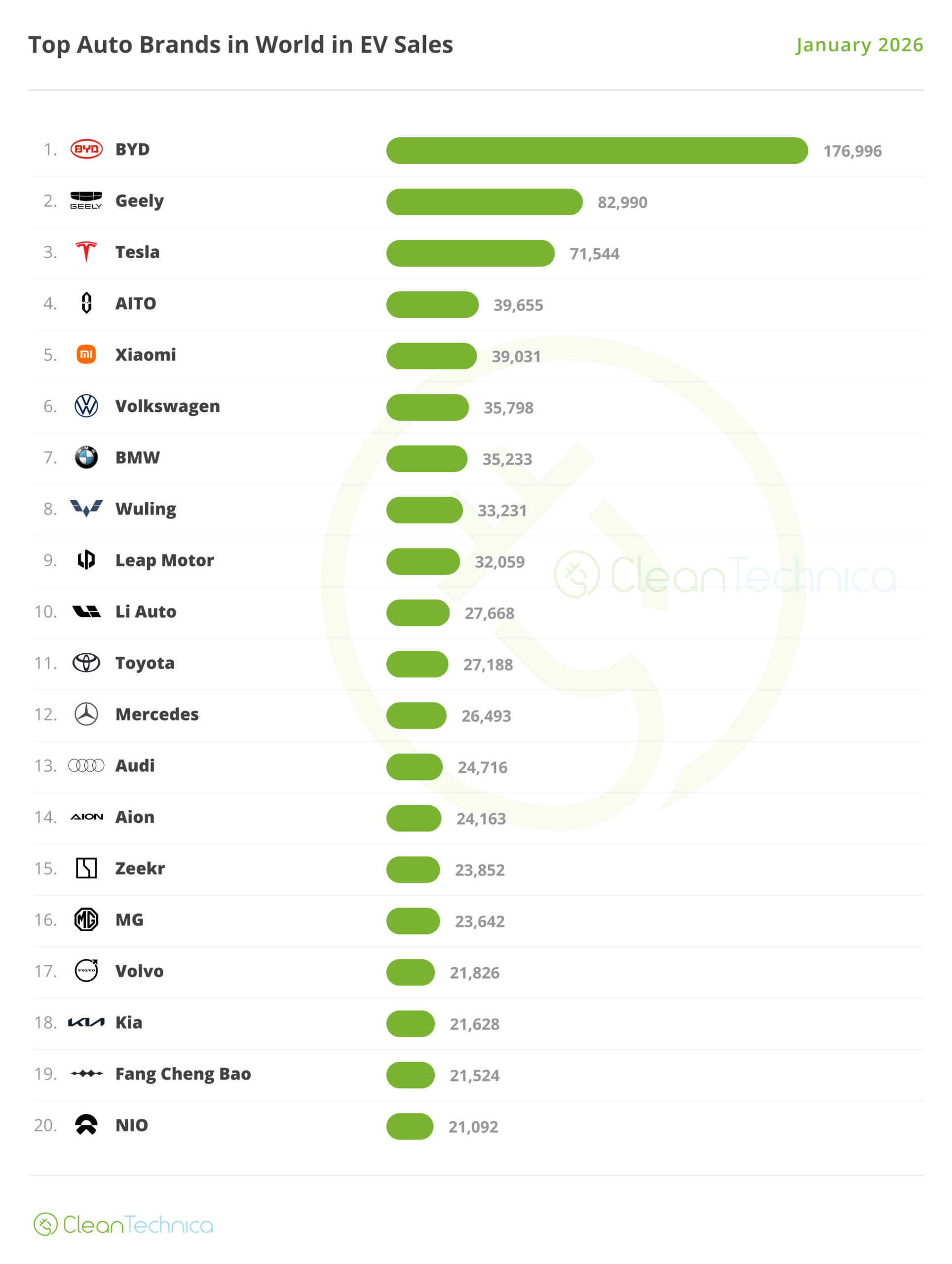

With two exceptions, January saw all top selling brands in the red, and not by small margins. BYD and Tesla dropped 21% YoY, Wuling crashed 30%, and Geely dropped by 12%, which is still a better performance than both Volkswagen (-14%) and BMW (-13%)….

Tesla’s performance was its worst since July 2022. Compared to January 2025, it is visible that the US brand is diversifying its markets, betting more on less mature ones. A year ago, 49% of Tesla deliveries were in the USA, 33% in China, 11% in Europe, and the Rest of the World (ROW) representing just 7%. Now its domestic market represents 47% of sales, China 26%, Europe 11% and the ROW 16%.

Now, about those exceptions I have mentioned before. While all legacy brands in the top 8 experienced two-digit drops in January, the two startups present had the opposite behaviour — #4 AITO jumped 82% YoY, thanks to the success of its new generation M7, while #5 Xiaomi is riding the wave of the YU7’s success, jumping 70% YoY last month.

And these two startups are still entirely dedicated to their domestic market. Imagine when they decide to go abroad….

Geopolitics aside, Xiaomi’s sporty ethos could be quite successful in Europe, while AITO’s big, comfy SUVs would feel right at home in the USA, don’t you think?

Brand

January

%

1

BYD

176,996

15.0%

2

Geely

82,990

7.0%

3

Tesla

71,544

6.0%

4

AITO

39,655

3.4%

5

Xiaomi

39,031

3.3%

6

Volkswagen

35,798

3.0%

7

BMW

35,233

3.0%

8

Wuling

33,231

2.8%

9

Leapmotor

32,059

2.7%

10

Li Auto

27,668

2.3%

11

Toyota

27,188

2.3%

12

Mercedes

26,493

2.2%

13

Audi

24,716

2.1%

14

Aion

24,163

2.0%

15

Zeekr

23,852

2.0%

16

MG

23,642

2.0%

17

Volvo

21,826

1.8%

18

Kia

21,628

1.8%

19

Fang Cheng Bao

21,524

1.8%

20

NIO

21,092

1.8%

Others

372,607

31.5%

TOTAL

1,182,936

100%

Regarding the remaining positions on the table, the biggest surprise was Toyota’s #11 position. Will 2026 be the year that the giant awakens?

I mean, it is strange to see the best selling automotive brand in the world not even making the top 10 among EVs….

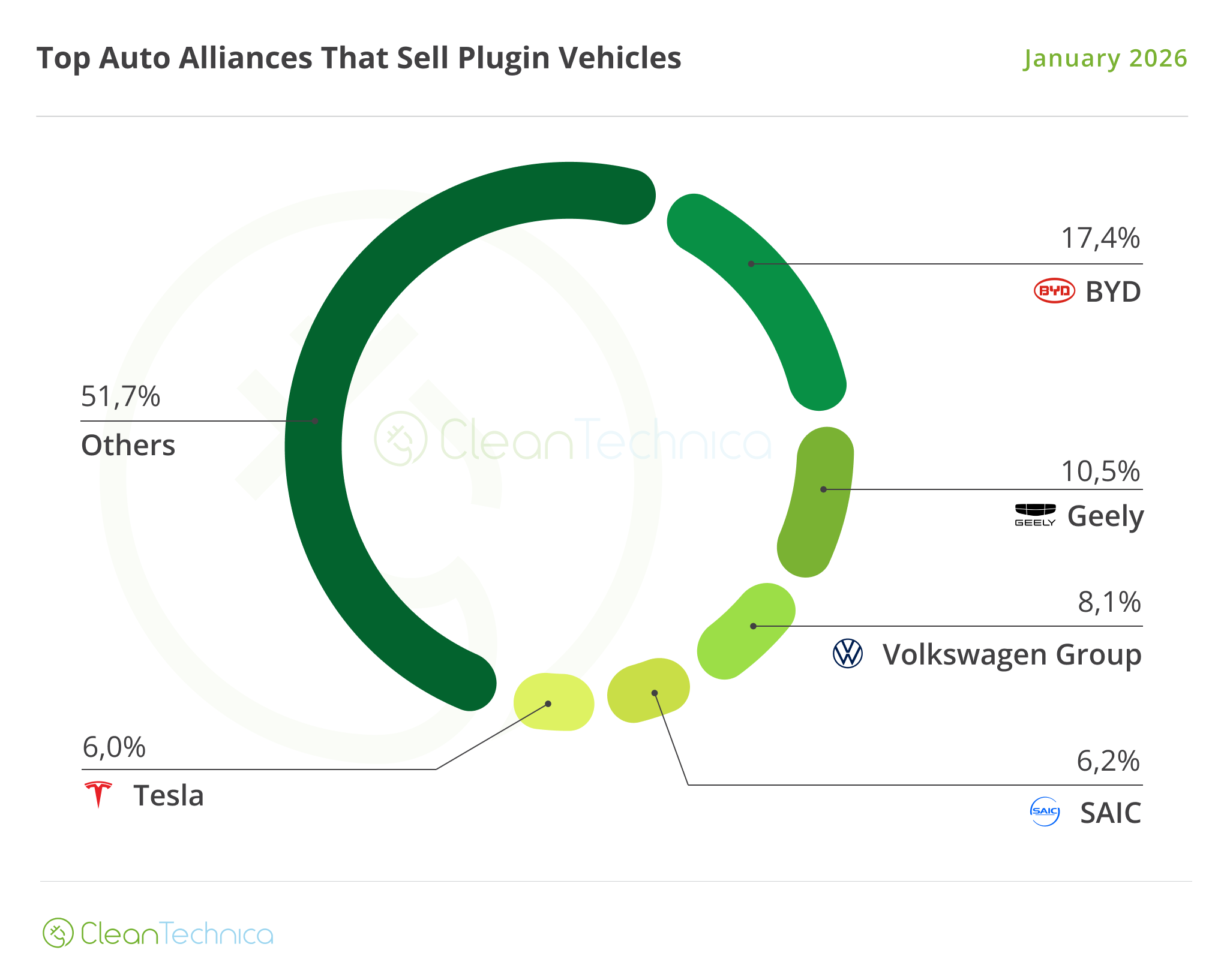

Looking at OEMs, BYD (17.4%, down from 23.6% in January 2025) is once again starting out ahead, but its leadership is being significantly eroded. And that’s even with runner-up Geely (10.5%, compared to 11.8% a year ago) also going down.

Below these two, something seismic has happened — Tesla went from 3rd placed a year ago, with 8% share, to 5th now!

Yep, its current 6% share wasn’t enough to keep #3 Volkswagen Group (7.2% a year ago vs 8.1% now) and #4 SAIC (5.5% then, 6.2% now) behind it.

Empires rise, empires fall. At this moment, Tesla’s management still believes it can play at the big boy table with two and a half models, compared to the dozens that the others have.

And here lies another reason why Tesla is stagnating and/or falling. People are different. They have different tastes, different needs … and like to have different choices. Preferably with regular updates. And that’s something Tesla has also neglected.

Instead of going after pipe dreams, like FSD and the like, if Tesla had been properly managed, it would have launched a new generation Model S around 2022 and Model X in 2023, both with 800V architecture; a compact platform would have been launched in 2024, at the latest, with hatchback and crossover versions; the Model 3 would have had a station wagon body since around 2022; and a proper 7-seat version of the Model Y with extended wheelbase would have been launched around 2024 (in Tesla’s defense, it has launched the 7-seat Y L in China … and it will be only a matter of time before it lands elsewhere). With this lineup, Tesla would have enough arguments to compete against the best of China. As it is, the company is just coasting on brand recognition and inertia.

But I digress. Outside the top 5, Hyundai–Kia (3.6%) took profit from the weak moment of Chinese OEMs to start the year in 6th, ahead of BMW Group (3.5%) and Chery (3.5%).

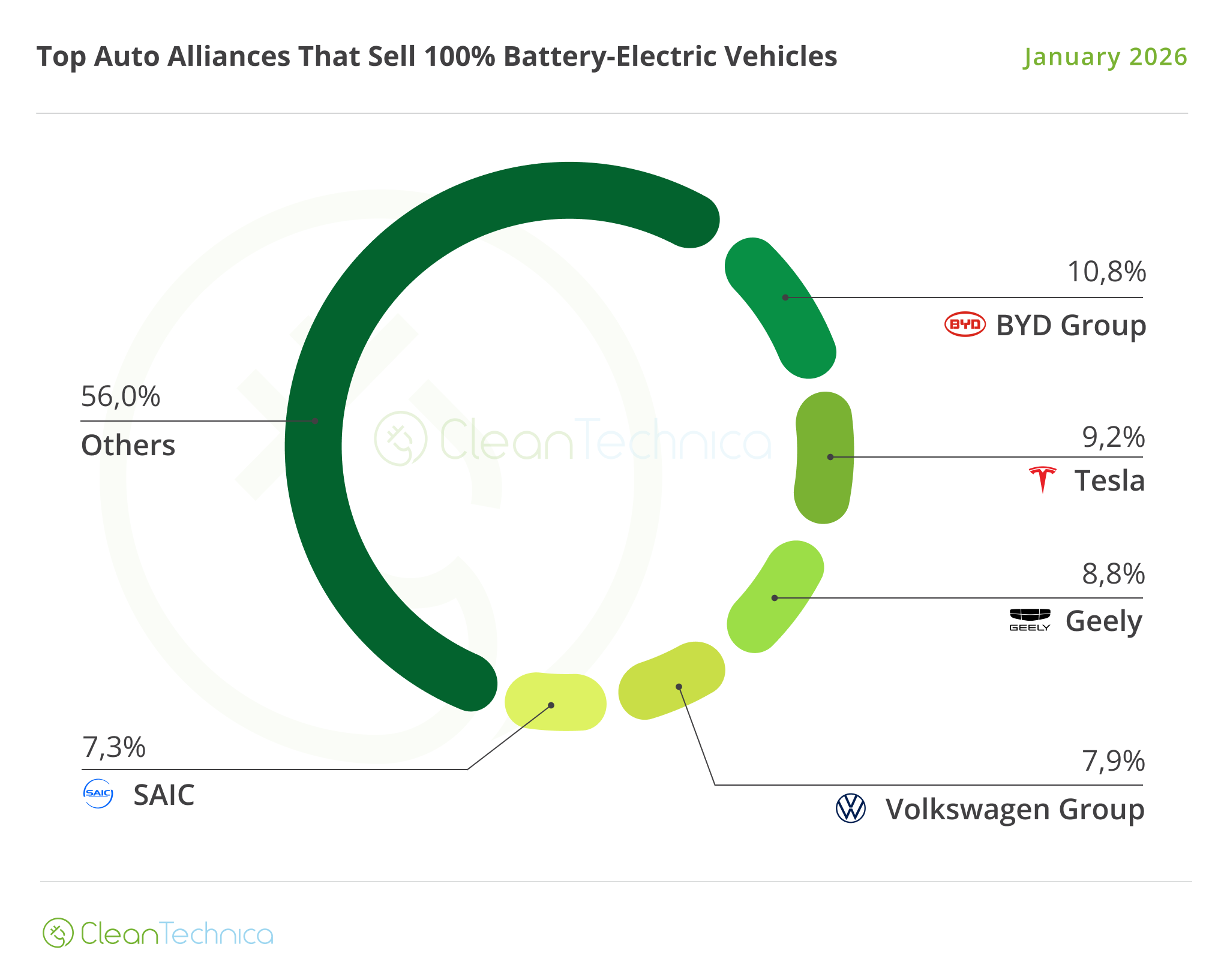

Looking just at BEVs, there were 774,191 registrations in January, or 65% of total plugin sales. BYD (10.8% share) started at the top, followed by Tesla (9.2% share, down from 12.4% in January 2025), which has narrowly beaten Geely (8.8%, down from 12.7% a year ago) in the silver medal position.

Off the podium, #4 Volkswagen Group started ahead (7.9% vs. 8.4% a year ago), keeping #5 SAIC (7.3% now vs. 7.2% then) behind it. Will the German OEM be able to keep SAIC behind it?

Outside the top 5, #6 Xiaomi (5%) is starting to gain a significant lead over the B League pack, with #7 Hyundai–Kia (4.3% share) already seeing the Chinese startup from a distance.

Will Xiaomi be able to reach the back of SAIC and Volkswagen Group this year?

Sign up for CleanTechnica’s Weekly Substack for Zach and Scott’s in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News!

Advertisement

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica’s Comment Policy