Valuation Check After Recent Pullback And Diverging Growth Narratives")

Tesla (TSLA) is drawing investor attention after its recent trading session, with the stock closing at $399.83 and showing mixed return patterns over the past week, month, and past 3 months.

See our latest analysis for Tesla.

The recent 1 day share price return of a 2.91% decline, on top of a 10.96% decline over 30 days and an 8.73% decline year to date, contrasts with Tesla’s 20.97% 1 year total shareholder return and 92.57% 3 year total shareholder return. This suggests near term momentum is fading while longer term holders have still seen substantial gains.

If Tesla’s recent swings have you rethinking where growth could come from next, it may be worth checking our screener of 34 AI infrastructure stocks as another way to look at the AI build out story.

With the stock at $399.83 and trading at only a small discount to the average analyst target of $421.73, the central question is whether Tesla is still undervalued or whether the market is already fully incorporating expectations for future growth in the current price.

Most Popular Narrative: 32% Undervalued

At $399.83 a share, the most followed narrative on Tesla, according to BlackGoat, points to a fair value of $588.18, which is materially higher than where the stock closed.

The Q4 results prove that Tesla can maintain 20%+ margins even while selling fewer cars, validating the shift away from pure volume chasing. The “Sum of the Parts” valuation model is being de-risked in real-time, but the stakes have never been higher. Tesla has burned the boats. It is now AI or bust.

This thesis starts from Tesla as a car maker and develops into a high conviction AI and robotics case. The narrative focuses on faster revenue expansion, rising margins and a premium future earnings multiple, and examines how these factors combine to reach a fair value that is well above today’s price.

Result: Fair Value of $588.18 (UNDERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, this bullish AI and robotics story could unravel if robotaxi rollouts face long regulatory delays or if chip supply constraints slow Tesla’s heavy compute build out.

Find out about the key risks to this Tesla narrative.

Another View: Pricing In A Lot Of Optimism

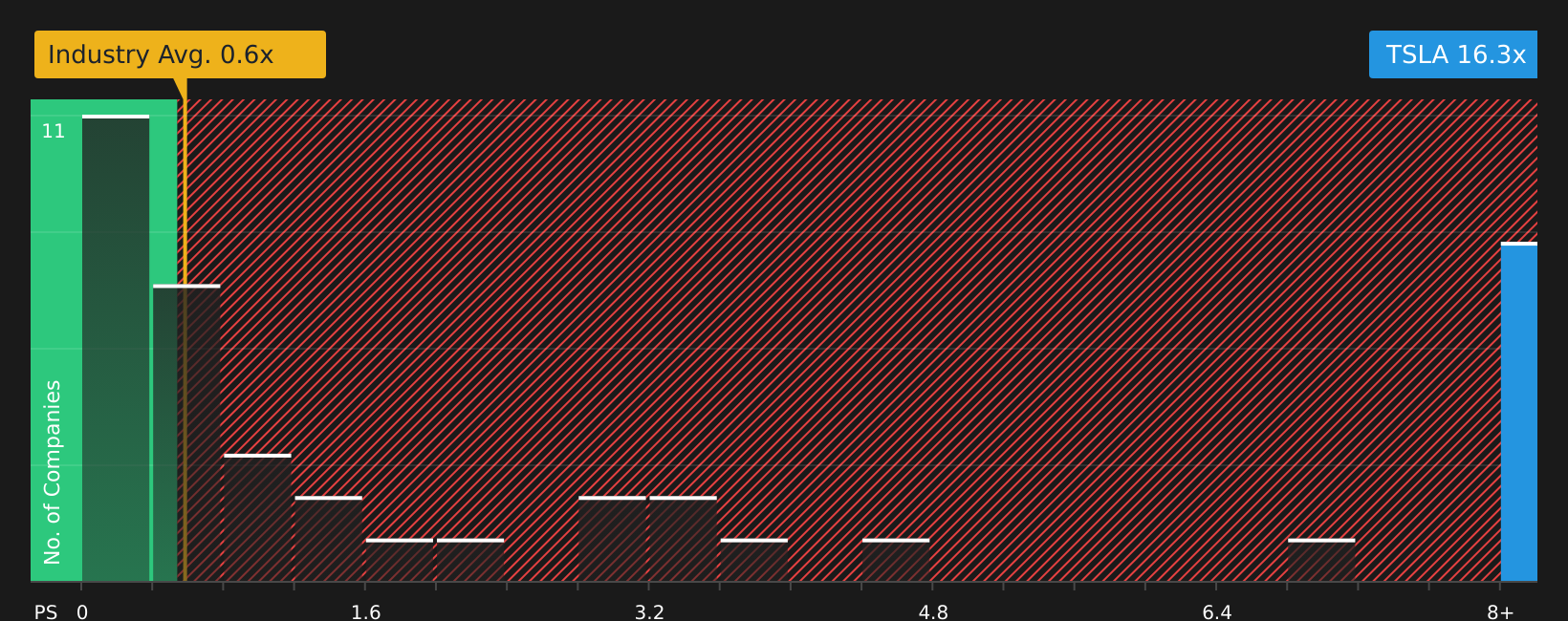

That 32% undervaluation narrative runs into a very different picture when you look at how the market is already pricing Tesla’s sales. At a P/S of 15.8x versus 0.5x for the US auto industry, 1.3x for peers and a fair ratio of 3.3x, the stock carries a lot of expectations. If those AI and robotics ambitions hit bumps, how much room is there for disappointment?

See what the numbers say about this price — find out in our valuation breakdown.

NasdaqGS:TSLA P/S Ratio as at Feb 2026Next Steps

NasdaqGS:TSLA P/S Ratio as at Feb 2026Next Steps

If this mix of confidence and caution around Tesla has you thinking, it is worth looking at the numbers yourself and moving quickly. To see how that balance of concerns and optimism stacks up in the data, take a closer look at the 1 key reward and 3 important warning signs.

Looking for more investment ideas?

If you are weighing what comes next after Tesla, do not stop at one stock. Use tools that help you compare different ideas side by side.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we’re here to simplify it.

Discover if Tesla might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com